Hybrid Ownership

Token design often fails to reward ownership to stakeholders in a way that aligns with how they uniquely provide value. Current designs grant the same form of ownership to all stakeholders, regardless of their role or value contribution to a protocol. This approach is potentially inefficient and limiting sustained user involvement over time. A solution is to explore a hybrid token model that assigns different forms of ownership based on the value contributed by users, founders, and investors uniquely. A hybrid model will allow for more efficient use of protocol capital and ensure that ownership rights can be given to users in perpetuity.

Most current token designs grant governance power and some claim on the future prosperity of the protocol. This appreciating token ownership concept is powerful because it is a claim on protocol growth, regardless of the owner’s actual future or sustained value. Outside of crypto, the risk of giving appreciating rights (e.g., stock or stock options) to stakeholders is managed through an interpersonal trust or legal contract and has understandably been limited to employees, investors, and the like. Each can be assumed to be long-term value aligned with and value-providing to the issuing company. A protocol has no contract or relationship with each of its users. Without some greater assurance, protocols are likely giving away too much on faith.

The counterpoint to appreciating ownership is one that is only historical and provides no claim on future growthor productivity. Cooperatives utilize a unique form of ownership structure called patronage capital. It allows members to share in the current year’s profit of the cooperative based on each member’s revenue contribution. Unlike traditional forms of ownership, such as stock or equity, which provide a claim on future growth or productivity, patronage capital is only a claim on the income of that single period, not a claim to anything in the future.

For example, if a cooperative has total revenue of $100 and a net income of $10, a member who contributed $10 of the protocol’s revenue during a period would be entitled to $1 of income for that period. Still, they have no rights to the income of future periods. This form of ownership is backward-looking, based on a member’s past actions. This historical conception is more appropriate for normal users doing normal user things. It rewards users for their past actions but requires them to stick around continually to be relevant.

Appreciating tokens that grant an interest in perpetuity are not to be avoided; they are another tool and one that is more appropriate for stakeholders where there is a high assurance about the long-term value they are providing. Initially, this type of ownership may only be appropriate to insiders (founders, employees, investors) but eventually may broaden to other stakeholders (i.e. users with demonstrated loyalty) over time. To understand what a hybrid model may look like in practice, consider the following token design for ABC Protocol:

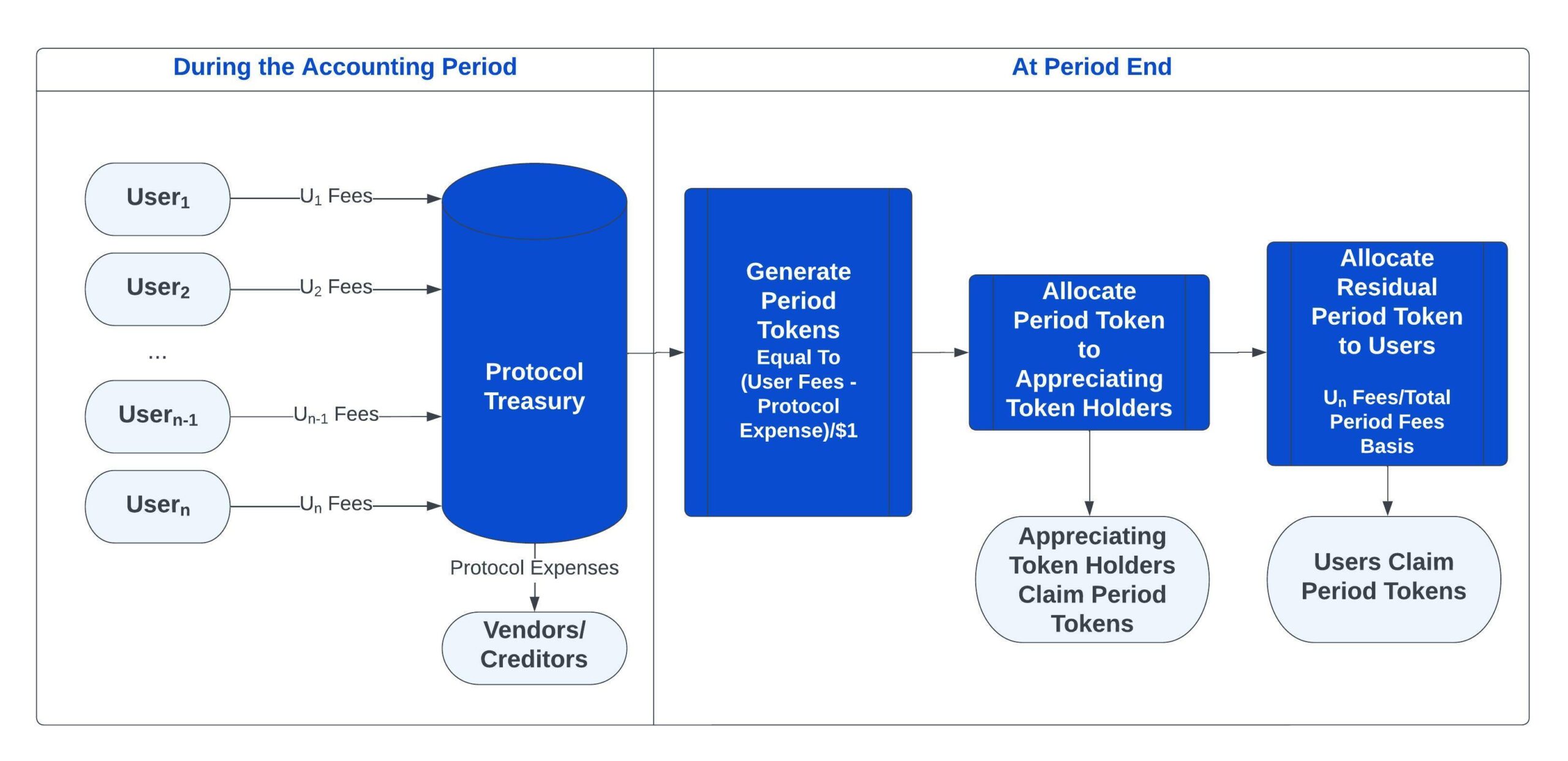

ABC’s founders determine the best on-chain metric of measurable value to be fees paid by the protocol users. At the end of each accounting period, the protocol calculates net income and generates one token for each dollar of income. This token is called ABCPeriod X token and represents a claim to a $1 dividend claim on the protocol, redeemable in the future at the discretion of governance, with preference given to tokens issued in earlier periods. Period tokens are issued at the end of every calendar year. Once the protocol has excess cash-flow governance can decide to retire period tokens, in order of issuance, by allowing the period token to redeem $1 equivalent of stable coins from the protocol treasury.

If this protocol were a pure cooperative ABCPeriod X tokens would then be distributed like patronage capital pro-rata to each user based on the value of their fees paid into the protocol. This model leaves nothing for founders, investors, or the like whose value is not captured in protocol revenue. The objective of the ABC protocol is to also redistribute profits to these stakeholders, which provide hard-to-measure value.

ABC’s founders accomplish this by issuing a second token to themselves, their employees, and investors. Each ABCAppreciating token is a claim on 0.0001% of ABCPeriod X tokens each accounting period (year) in perpetuity. ABC has a required insider reserve of 25%, so at protocol launch 250,000 ABCAppreciating tokens are distributed to founders, early employees, investors, and future employees. ABC protocol is also set up so that governance can issue up to 250,000 more ABCAppreciating tokens to distribute to others providing value outside of protocol fees post-token launch.

Each time ABCPeriod X token is generated, ABCAppreciating token holders are allocated their claim percentage and the residual is allocated to users based on their proportionate share of fees paid into the protocol, similar to a patronage dividend.

Normal users of the ABC protocol earn historical ownership by using it; they do not profit from token ownership, but are in effect guaranteed the lowest costs to use the protocol through patronage dividends in the form of ABCPeriod X tokens. At the same time, founders and investors continue to have the significant upside of appreciating tokens to incentivize growth outside the direct measurable value metric.

Suppose a hybrid model includes a token tied to a specific period or milestones like the ABCPeriod X token, it allows for the continual renewal of governance and greater assurance that a protocol is always close to its current users. A protocol can achieve this by tying governance to the period/milestone token and setting governance power to decay on some schedule. Resuming our example of ABC Protocol:

ABC founders designed a protocol where governance power decays over time and ABCPeriod X tokens are the governance unit of the account. ABC protocol is initially set up to such that the ABCPeriod X tokens governance weight is based on a declining geometric series dependent on the age of ABCPeriod X tokens. In year Y, ABCPeriod Y-1 tokens are given ½ the total weight, ABCPeriod Y-2 tokens ¼ the total weight, and so on. As time passes each historical period’s governance power diminishes but the $1 dividend claim remains the same.

To be clear this is one of many approaches to the following questions:

- How do we give users ownership sustainability over long time spans?

- How do we design tokens that allocate ownership effectively?

- How do we keep current users governing the protocol?

There are already teams out there thinking and implementing thoughtfully on these types of questions. For example, Goldfinch is paying membership rewards and giving additional governance power to token holders who demonstrate long-term loyalty by locking up tokens and financing capital valuable to the protocol. The Canto network is gearing up to launch Contract Secure Revenue where developers can opt-in to earn a percentage of gas paid to the network when users interact with their smart contracts.

There are more nuanced advantages to this model as well. The legal classification of period tokens may be advantageous to founders. Period tokens are fixed cash claims on the protocol, not a claim on its future expected performance, or its founders. We can also be assured the distribution of period tokens to normal users is never in amounts greater than the value (fees) they provide to the protocol. There can be no expectation of profit either before the period token is extant or afterward, and there are no future additional dividend rights. This fact pattern could reduce, but maybe not eliminate, the risk of period tokens being considered a security. There is no diminished risk in relation to appreciating tokens in this structure, but this may allow founders to distribute historical ownership to the community via period tokens much earlier and let the community issue appreciating tokens to non-insiders after the protocol is fully decentralized.

Users have to come and stay for the product. Ownership should be an enhancing part of their experience rather than the whole of it. A hybrid model is not the best model for bootstrapping new users because there is no expectation of outsized future profit, it does not excite the same type of greed, but I believe is sustainable in the long run and does a better job of keeping protocols governed and owned by their users.

Token design is in its Precambrian, single-celled state. At Variant, we want to work with individuals and teams building sustainable protocols that will last to mainstream adoption. Reach out to us if you are thinking deeply about alternative governance systems.

Big shout out to Nathan Schneider, Li Jin, Jesse Walden, Spencer Noon, and Alana Levin for the help and ideas. This essay was also published on my Mirror.

1This rate of decay is just a simple example, the actual function would at least be dependent on the length of the period selected and optimized for short-term governance risks.

2If you wanted to take it one step further you could issue period tokens so that they were non-transferable or had limited transferability.

***

Disclaimer: This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.