Crypto as the Next Iteration of the Attention Economy

Memecoins, NFTs, and tokens are new “attention assets” that measure the value of attention in real time

This post first appeared in Li’s newsletter.

Last week, an NFT of Achi, the original dog wearing a hat, sold for 1,210.8 ETH ($4.3 million USD) on Foundation. And just yesterday alone, over 5,000 new memecoins were launched on Pump.fun, each one an asset that encapsulates an idea that others can invest in. These are examples of how crypto translates attention value into economic value—and enables a more efficient attention economy.

Web2 as a failed attention economy

The term “attention economy” has gained major traction over the past several years, but it traces its origins to the 1970s and social scientist and Nobel laureate Herbert A. Simon. Simon observed that “a wealth of information creates a poverty of attention.” Attention is a scarce resource, with dynamics of supply and demand surrounding it.

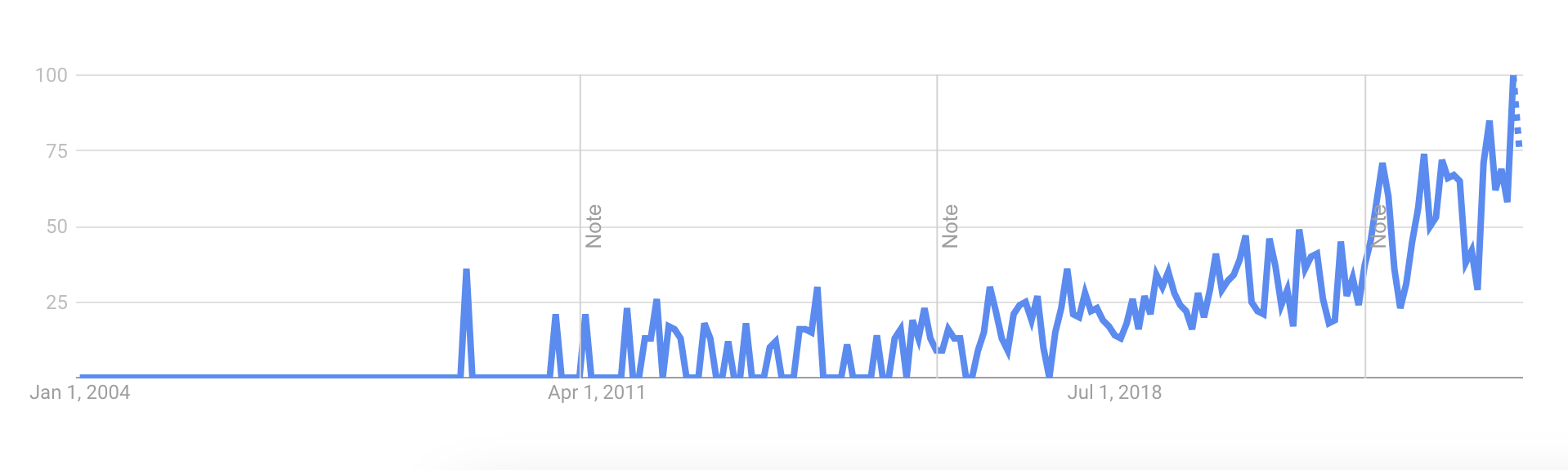

Interest in the attention economy over time

People commonly refer to web2 as “the attention economy,” where platforms compete intensely for user attention and treat attention as a commodity to be monetized; but the web2 attention economy is plagued by rampant value leakage, with positive and negative externalities.

In economics, the concept of an “incomplete market” refers to situations where certain markets are missing or inadequate, leading to inefficiencies and misallocation of resources. The web2 attention economy is one such incomplete market, where there are insufficient mechanisms to measure attention (its quality and intensity) as well as a lack of financial instruments to facilitate its value capture.

Advertising, the dominant business model of web2, is a suboptimal way to capture value from attention: attribution is imperfect, and certain types of value aren’t adequately captured by ads. Advertising favors closed loops and actions that take place on a short time horizon, whereas there are some forms of value—for example, career guidance or other forms of knowledge transfer—that are less obvious, or require longer time horizons to be realized.

Among creators, the inability to fully capture value from their attention manifests in a host of emerging monetization mechanisms, from branded products to coaching to courses. But these all likely still leave money on the table. Think of popular creators from Mr. Beast to Charli D’Amelio—they monetize their fans’ attention through sponsorships, restaurant chains, and television shows, but also only capture a fraction of the value they create, because those products don’t fit every audience member. That’s not to mention creators who provide significant value to a small base of users, whose attention “quality” is better, but find it challenging to monetize through dominant means.

The web2 attention economy has its shortcomings for users as well. A common refrain in web2 is that “if something is free, you are the product.” (Interestingly, the phrase also has its origins in the 1970s, with artist Richard Serra saying it about television). The dominant business model for web2 platforms is to amass as much data about users as possible, such that they can be more effectively targeted for advertising. In other words, the value that users’ attention brings is being harvested by platforms, rather than flowing to users.

Crypto and attention assets

Crypto can be viewed as the next iteration of the attention economy, with a much more efficient market. Memecoins, NFTs, and tokens (as well as new asset classes) can be considered new “attention assets,” measuring and capturing the value of attention in real time. Users can invest and own attention assets as a way to express their beliefs about whether that particular meme, media, creator, or network will accrue more attention and interest in the future. When users invest in memecoins, they are implicitly making a statement that they believe that particular token and meme will grow in popularity: attention is the primary driver of value. One X user called memecoins “a way to angel invest in culture.” Platforms like Perl, Fantasy.top, and Friend.tech have created new financialized markets around attention, allowing users to profit based on whether they correctly guess which assets, creators, or content will succeed in garnering more attention.

This can also work in reverse: tokens can help to incept attention initially, forming a speculative community that can pave the way for more organic interest later on. DEGEN is an example of this. It launched in January 2024 to the Farcaster community and appears to be a community currency for rewarding quality content on the network. Outside of the memecoin world, this pattern of using tokens to bootstrap attention has precedent in decentralized physical infrastructure networks (DEPIN) like Helium and Hivemapper, as well as in the web3 creator economy.

A more efficient market is a market that better serves the needs of stakeholders on both sides of the value exchange. I’ve written extensively about how crypto assets can restore scarcity to the digital landscape and capture users’ full willingness to pay. And for users, crypto creates the opportunity to own attention assets and become the beneficiaries of the attention that a given thing is garnering, whether that “thing” is a meme, song, community, network, or protocol. The user shifts from the product that is being sold by a platform, to the owner of a unit of attention that has value and can appreciate over time.

The attention economy has undergone evolutions with the rise of user-generated content and digital platforms, and AI-generated content only represents a further catalyst for more demands on users’ attention. The difference from the web2 to the web3 iteration of the attention economy is that in web3, everyone in the value chain can benefit from being owners of attention assets—whether they originated the object of attention, or merely paid attention early.

+++

This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.