DePIN and DeREN: Toward a Better Classification of Decentralized Infrastructure Networks

With the rapid expansion of decentralized infrastructure networks, it’s worth redefining these networks into two categories based on their unique properties.

Decentralized infrastructure networks—cryptonetworks that leverage token incentives to generate the liquidity to fund physical infrastructure operations—are proliferating fast.

The value of these networks is clear: they offer a better solution for powering consumable resources, from computing to energy to data. In turn, these resources are directly consumed by companies or, more often, leveraged in their own products and services. For instance, decentralized networks like Hivemapper sell data directly to transportation companies like Uber, which in turn use the imagery data to improve their product offerings. Similarly, Livepeer enables livestreaming applications to tap into its marketplace for video transcoding services but is also integrated by companies like Bonfire, which lets creators easily spin up their own livestreams.

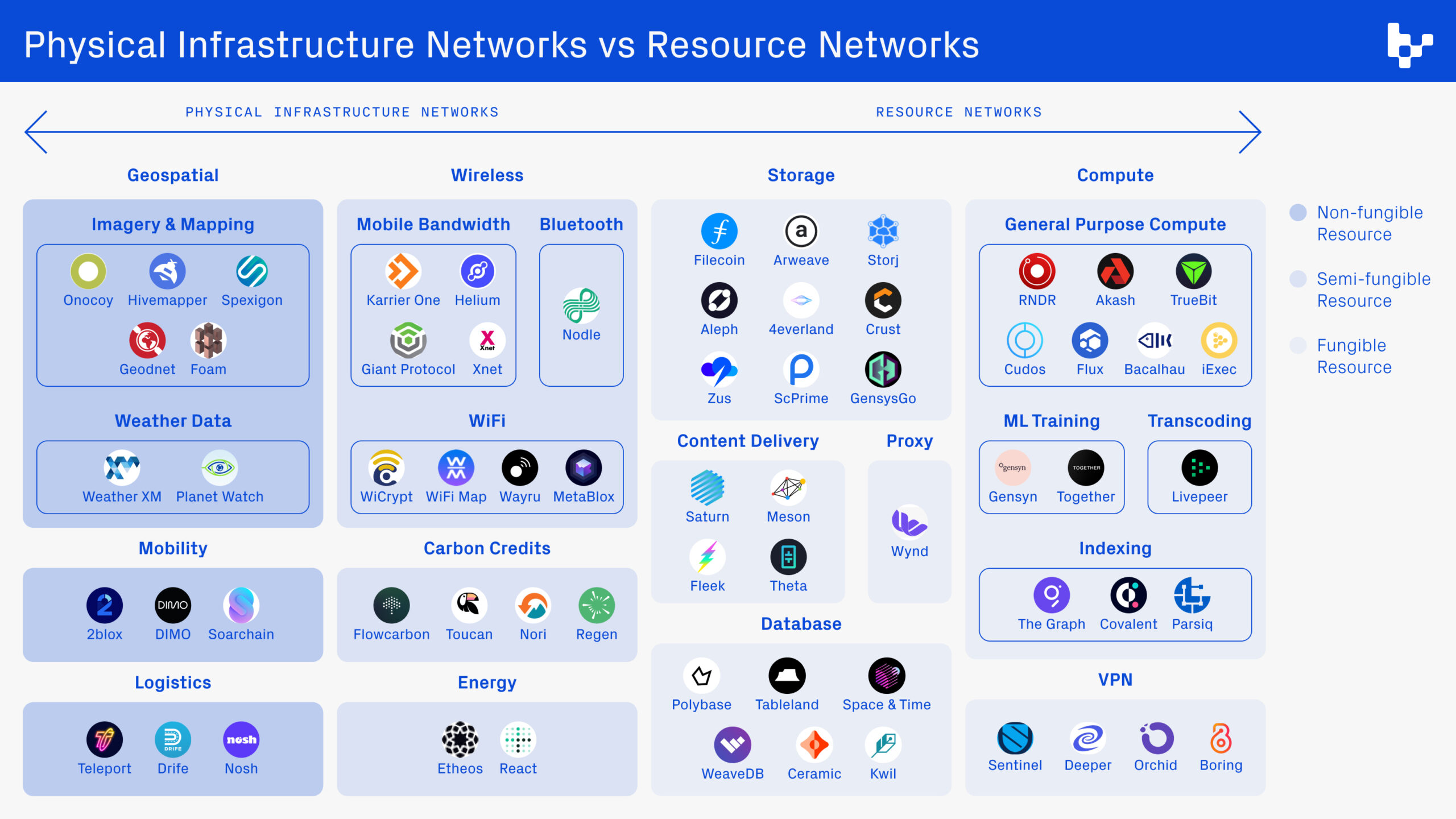

To better evaluate the potential of these networks, we need a better way of categorizing them. The current sector name that has caught on is DePIN (coined in 2022 by the folks at my former employer Messari), but I suggest introducing further granularity and splitting decentralized infrastructure networks into two groups:

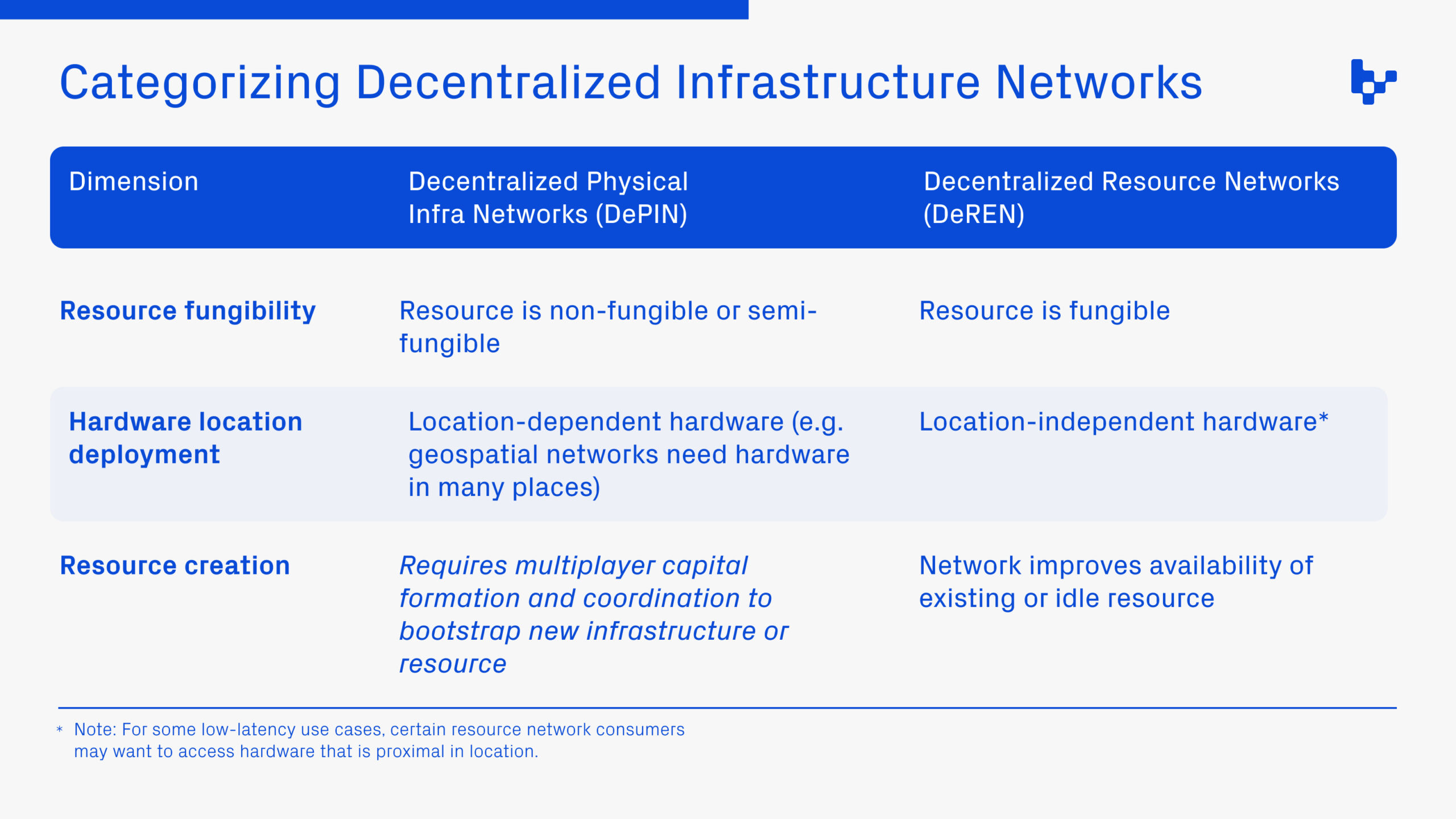

- Decentralized physical infrastructure networks (DePINs): cryptonetworks with consumable, non-fungible resources that leverage incentives to deploy location-dependent hardware devices

- Decentralized resource networks (DeRENs): cryptonetworks that leverage incentives to build marketplaces and increase the supply of existing or idle consumable, fungible resources that rely on location-independent hardware

DePINs differ from DeRENs across three core dimensions:

- Resource fungibility

- Hardware location deployment

- Resource creation

Resource fungibility

The most meaningful of the above differences is the fungibility of the consumable resource.

In resource networks, the consumable resource is fungible because the network’s hardware assets are typically interchangeable. For example, the computational resources provided by networks like Akash or Render are highly fungible—the processing power of one GPU is the same as any other GPU with the same specifications and capacity. With the exception of highly specialized activities like high-frequency trading, users typically do not care where their hardware is deployed geographically, so long as the network latency is acceptable compared to centralized architectures.

Conversely, DePINs leverage non-fungible or semi-fungible resources. In such cases, the consumable assets are not easily interchangeable and hardware is often unique to a particular network. For instance, Hivemapper’s dashcam maps a specific location, which produces data unique to that location and place in time. Further, an imaging network like Spexigon cannot contribute its aerial image data to the Hivemapper network; the asset of each network is image mapping data, and it’s exclusive to that network.

There are, of course, assets in the middle of the spectrum. Energy, for instance, is semi-fungible because it can be used for a variety of purposes but its utility is limited by the distance of transmission.

Hardware location and resource creation

Hardware location and resource creation are closely related; the deployment of application-specific and location-dependent hardware often coincides with building a proprietary resource.

On this count, DePINs face more challenges building both the supply and demand sides of a market. The supply side requires location-dependent hardware setups, while generating demand depends on there being enough scale on the supply side to make the network valuable to consumers.

It is easier for resource networks to bootstrap supply since the idle supply can come from anywhere and often doesn’t require the creation of new hardware and infrastructure. But resource networks with fungible assets also face greater competition since the cost of switching from one resource network to another is lower.

Building moats in DePINs and DeRENs

Crypto-based resource networks must still compete with their web2 counterparts like AWS and Google. While DePINs and DeRENs can leverage tokens to subsidize initial resource costs, the most successful networks won’t compete on price alone, but instead will unlock new demand or expand the market in unique ways.

Arweave, for instance, didn’t compete on file storage pricing. It offered new functionality and convenience through permanent storage and eventually found traction storing NFT metadata. In the DePIN category, mobility networks like DIMO aggregate previously siloed data that power a new wave of applications, from battery intelligence and energy management to better vehicle commerce.

Another successful strategy is to vertically integrate and generate demand by building the initial product that leverages the infrastructure or resource network. Render couples its GPU-rendering capabilities with its Octane software, which drives usage of the underlying compute resource network.

If you’re building new resource networks or physical infrastructure networks that create demand for new users and applications, I want to hear from you: [email protected].

Thank you to Jesse Walden, Sami Kassab, Dustin Teander, and Alana Levin for feedback, comments, and conversations that helped develop many of these ideas.

+++

Variant is an investor in DIMO and Bonfire. This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.