The Next Frontier in Cryptoeconomic Business Models

Originally coined in the 1990s by Clayton Christensen, disruptive innovation – innovation that enables a new market entrant to outcompete an incumbent – occurs when a new technology is combined with an innovative business model. Crypto, like every emerging technology, is full of breakthrough technical innovations (including cryptography, mathematics, finance, and computer science). The abundance of technological innovation often means that the disruptive innovations in crypto tend to come from protocols and companies that implement new cryptoeconomic models or distribution mechanisms.

By following emerging trends in token distribution and cryptoeconomic model innovation – two components of crypto business models – we can attempt to answer the question, “where will the next wave of disruptive innovation in crypto originate from?”

How Token Distribution and Cryptoeconomic Model Drive Innovation

Blockchain networks offer a blank canvas for token distribution and cryptoeconomic models. Bitcoin’s cryptoeconomic model – proof of work – sparked a variety of new PoW currencies, most notably Zcash and Ethereum. And while Ethereum offered a variety of technical innovations compared to Bitcoin (i.e., Turing completeness, smart contracts, etc.), Ethereum’s first killer app wouldn’t be popularized until 2017, when initial coin offerings (ICOs) leveraged smart contracts and the ERC20 token standard to trustlessly distribute tokens to participants. This token distribution model has been so critical to the growth of web3 that we’ve seen further iterations of the core concept: initial exchange offerings, initial DEX offerings, liquidity bootstrapping pools (LBPs), automated crowdfunding platforms (e.g., JuiceboxDAO), and more.

NFTs were yet another interesting technical innovation, but didn’t truly explode until the deployment of NFT marketplaces like SuperRare, LarvaLabs, and OpenSea that facilitated the transfer of on-chain royalties.

Another great example of the power of business model innovation compared to technological innovation is in respect to ZK technology. The race to scale Ethereum has driven billions of dollars into zero knowledge research, spawning impressive technical developments across a variety of approaches. To date, ZK rollups (like Aztec, Scroll, Zksync, and Hemez) have been drivers of various breakthroughs. Now, the next wave of Ethereum scalability solutions will be driven by design innovations in cryptoeconomic models that incentivize ZK sequencing, proving, attestation, and network value capture.

The Next Wave of Crypto Economic Models

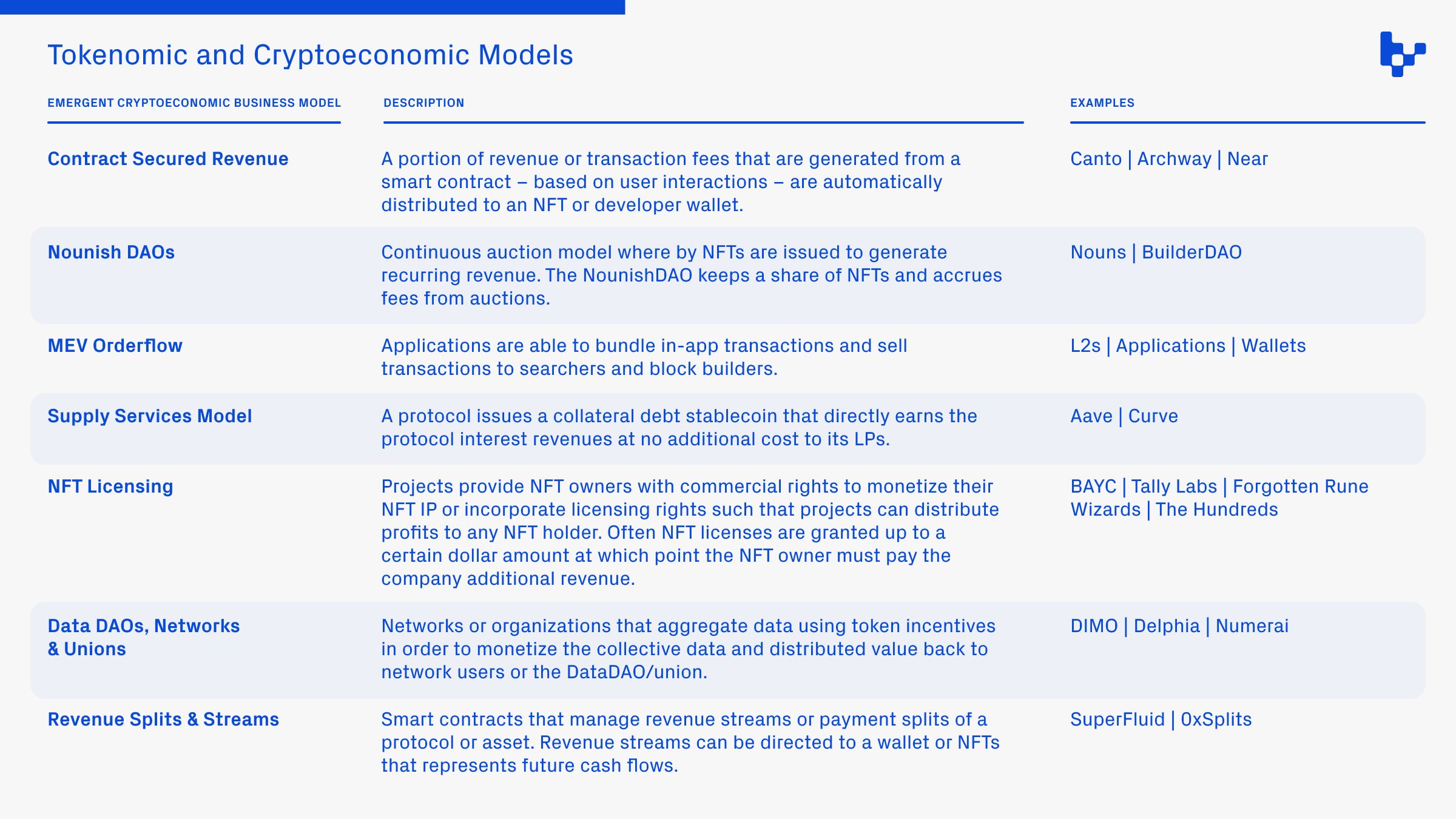

Each wave of crypto is dominated by new distribution mechanisms and cryptoeconomic models, so let’s examine three of the newer emerging models: Contract Secured Revenue, NounishDAOs, and MEV Orderflow.

Contract Secured Revenue (CSR)

Contract Secured Revenue is when a portion of fees from the utilization of a smart contract accrues to an NFT or an address (e.g., developer). On Ethereum, fees for interacting with smart contracts are burned and the protocol generating the usage receives no reward for creating the value, other than the revenue from any app-specific transaction (e.g., NFT marketplace fee). Layer-1s like Canto utilize CSR as a core primitive to align developers and economic activity. Importantly, CSR NFTs can accrue fees from multiple smart contracts (e.g,. smart contracts on different versions of a protocol).

Another L1 on Cosmos, Archway, similarly rewards applications on the network. More specifically, Archway offers three configurable rewards distribution mechanisms: gas rebates (50% of rewards go to developers), inflation rewards (25% of which go to app developers), and smart contract premiums (e.g., custom fees).

This model – rewarding developers or protocols based on utility – offers a unique approach that doesn’t necessarily require a governance token to act as a claim on revenue or demand that a protocol take an additional fee on top of the network’s gas costs. Further, CSR as an economic business model potentially reduces the middleman take rate and further aligns a protocol that builds on top of an L1/L2 or an application that generates significant demand on top of an existing protocol.

More interestingly, it’s possible to adapt this model to any type of application where a portion of demand or usage-based revenue should be directed to stakeholders, creators, developers, users, etc). Imagine if TikTok’s Creator Fund – which is an important part of how creators earn money – was instead instantiated as CSR, whereby a portion of inflationary rewards or ad revenue was directly distributed to content creators based on view count or time watched on the platform. CSR offers a business model that can further align applications built on top of protocols.

Nounish DAOs

As NFT royalties face an uncertain future, two important questions loom large: where will recurring revenue for NFTs come from, and what is the optimal NFT business model? Nounish DAOs – projects that leverage the Nouns auction model to continuously sell NFTs – present one model for a subset of communities that are united by a common goal or can align around a capital formation and distribution. Nouns Builder enables anyone to create a Nounish DAO in minutes and has already supported the creation of dozens of new Nounish DAOs since its launch.

Perhaps most notably, many of the early Nounish DAOs formed via Nouns Builder aren’t focused on proliferating the Nouns meme:

- ArtHaus – a Nounish DAO focused on partnering with artists for drops that will launch from the ArtHaus DAO

- Spores – a Nounish DAO focused on creating the next-generation remixing devices for on-chain music

- BLVKHVND – the first DAO to win a professional world championship has now transitioned into a Nounish model

The Nouns mechanism isn’t suitable for every type of organization. Jacob Horne – cofounder of Zora and Nouns Builder – hypothesizes that the Nouns model is most efficient when applied to a general purpose as opposed to a specific application. One core component of this hypothesis is that a NounishDAO is most effective when it can fund competing approaches to achieving a broad goal, and is typically less useful for betting on a specific way to achieve a goal.

Source: Jacob Horne

Source: Jacob Horne

Take the following examples of broad vs specific goals:

- Proliferate the Nouns meme vs. create a Nouns movie

- Create renewable infrastructure vs. build a solar farm

- Consume carbon vs. buy carbon credits

There are a few existing categorical use cases for Nounish DAOs:

- Brands, Memes, and IP

- Membership

- Thematic funding or investments

- Creation of SoV assets (e.g. art)

As the Nounish DAO model modularizes, it has already started to offer features like non-CC0 IP (for other brands and IP), minimum NFT buys (for larger scale funding requirements), splits (e.g., share funding among other DAOs), and others. These additions and broader experimentation will expand the class of communities and DAOs that leverage the Nounish model.

MEV Orderflow / PFTF (Payment for transaction flow)

As MEV unbundles into multiple stakeholders (i.e. searchers, block builders, and proposers) applications that control users – and therefore transaction flow – will be able to bundle user transactions and sell them in private mempools to searchers and block builders.

Similar to how Robinhood pioneered payment for order flow (PFOF) to funds and institutions, applications (such as wallets and DEXs) will be able to adopt a payment for transaction flow (PFTF) to block builders. As MEV continues to grow as a category – and the opportunity for multichain MEV expands – rollups, appchains, and super dapps will look to MEV as a new revenue line. Another potential end state is these PFTF earning applications will redistribute their MEV orderflow revenue, in part, back to users in the form of gas subsidies or other discounts.

MEV will continue to be an integral part of the crypto. As applications and protocols make product decisions with MEV in mind, we’ll likely find MEV become increasingly important as a bottom-line revenue stream and as a core component of emerging business models.

Toward Better Web3 Business Models

The truth is that web3 has yet to standardize its era-defining business model. The most successful applications today have relied on web2’s transaction-based models – DEXs, marketplaces, etc. It’s likely that these models will remain popular (and profitable), but the ability to program and tokenize value also invites the potential for new business models. New token distribution mechanisms and cryptoeconomic models will act as the critical catalysts for the next wave of experimentation and disruption.

Thank you to Li Jin, Derek Walkush, and Medha Kothari for providing feedback and informing my thinking on many of the cryptoeconomic models in this piece. You can find more of my writing on both the Variant website and my blog.

***

Disclaimer: This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.