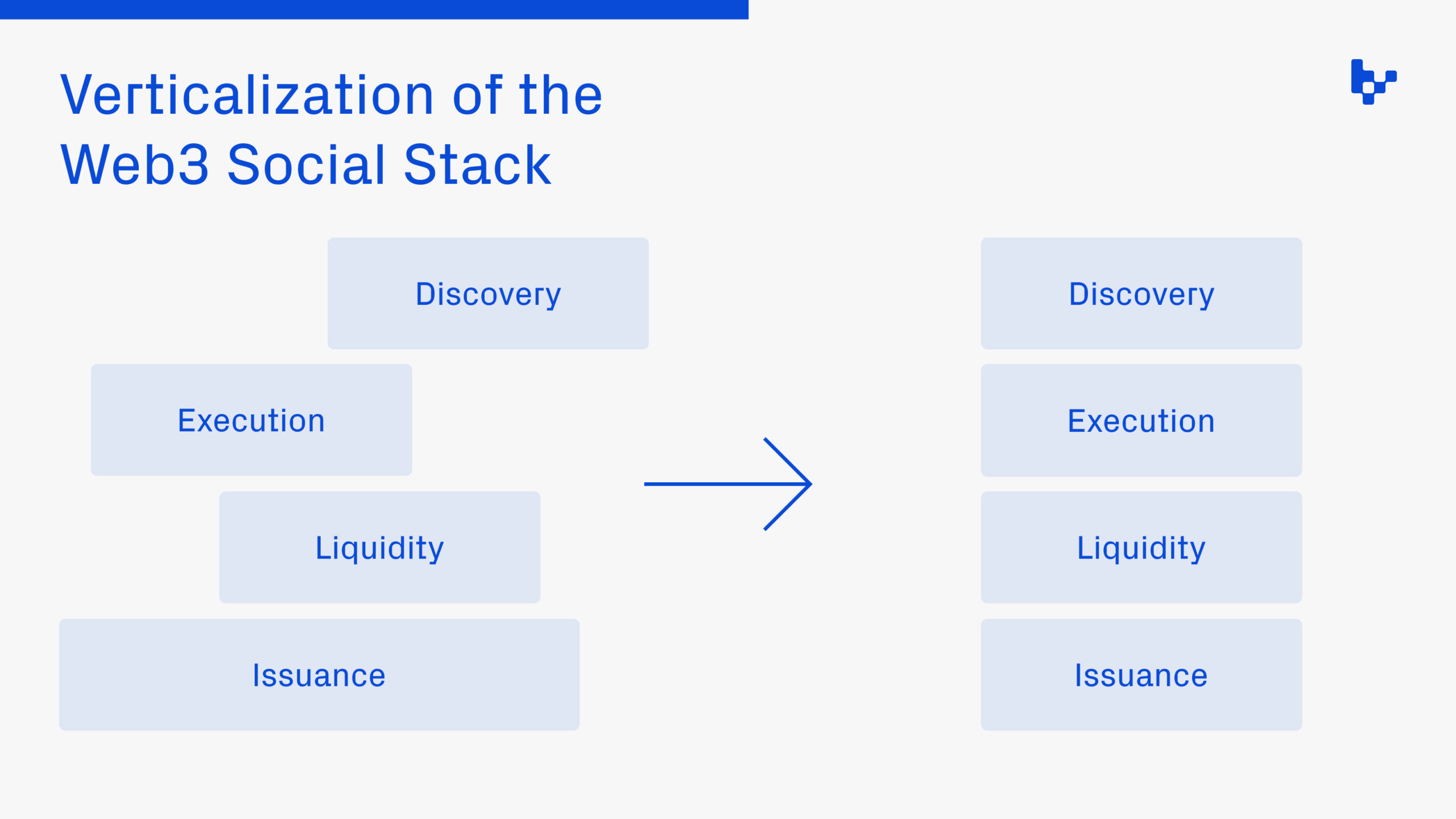

Verticalization of the Web3 Social Stack

As usage of crypto social platforms and financial games increases, the way they are constructed will continue to evolve. We can expect to see a trend towards increasing verticalization, with projects seeking to offer a more seamless and comprehensive experience for users that enables the creation of new consumer behaviors and attention or social-based assets. While not all web3 social experiences are financial, the blockchain rails that underpin crypto consumer applications allow for new token-incentivized behaviors and digitally native assets to be imbued into the social experience.

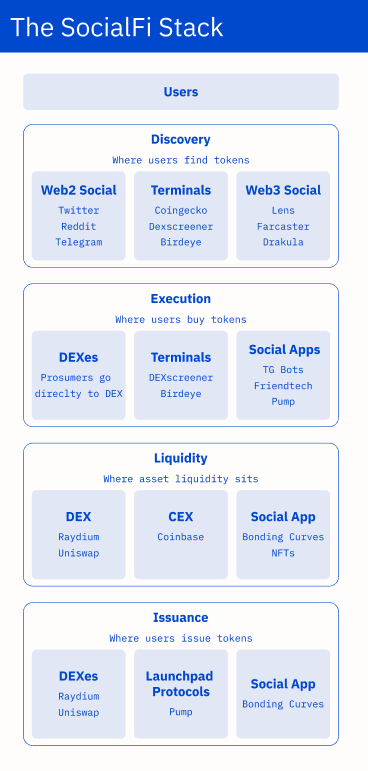

The existing SocialFi stack is comprised of four core layers:

- Discovery – where people discover what to buy

- Execution – where assets are bought and sold

- Liquidity – where assets reside and are pooled

- Asset issuance – where assets are created

Today, the stack is fairly fragmented, with the user discovery and social experience decoupled from execution (e.g. trading), liquidity, and asset issuance. But as the SocialFi frontier expands, applications will continue to verticalize attention and markets in an effort to control user social experiences and attention-asset liquidity.

SocialFi app builders will need to own multiple layers of the SocialFi stack in order to build protocol defensibility. Attention-asset trading (e.g. execution) and issuance are commoditized layers of the stack—token issuance is increasingly easy, and execution can be added anywhere that owns eyeballs. Owning either the discovery or liquidity layer will be of increasing importance since these are defensible layers of the SocialFi stack that exhibit strong network effects.

Within SocialFi, most applications are choosing between two approaches towards verticalization:

- Exchange-first approach: Build an exchange or marketplace where users trade attention assets (e.g. Robinhood for memes) and evolve into a social/discovery platform from there

- Social/discovery-first approach: Build a social platform to own discovery and then layer in financial elements and primitives with consumers/attention merchants as a key stakeholder in the platform

Exchange-First

Any social network or discovery platform faces significant headwinds: bootstrapping new social graphs, spurring new consumer behaviors, and retaining user engagement in an era of a hyper-competitive attention market. Given these obstacles, the exchange-first approach is arguably easier to jumpstart because users’ appetite for speculation helps to surmount those headwinds. However, this approach faces more competition because of the ease with which exchanges can be bootstrapped compared to social networks and the benefits that social networks retain once a threshold density has been reached.

From the exchange-first approach, deep verticalization of the SocialFi stack has proven effective because exchange-first applications have attention-trading capabilities built in. For instance, Friendtech has emerged as one of the most vertically integrated SocialFi apps, with control over the entire stack. The app serves as the focal point for key discovery and exclusive execution, and it leverages a native financial primitive––a bonding curve––that issues assets with utility specific to the Friendtech app.

Newer SocialFi protocols have also vertically integrated the SocialFi stack. For example, memecoin issuance and discovery platforms like Pump and Ape Store allow users to easily deploy a memecoin on a bonding curve. This enables users to easily purchase tokens directly from the bonding curve, as opposed to having to wait for someone to seed liquidity into a DEX or liquidity pool. While some Pump-initialized memecoin execution and discovery can occur on other platforms—DEX Screener and Twitter, respectively—protocols like Pump still provide a unique social discovery experience and execution platform for newly launched tokens.

Discovery-First

Historically, the discovery-first SocialFi approach has seen success through the likes of Twitter, Farcaster, and Telegram and also through market terminals like DEX Screener and CoinGecko. Many of these applications have tried to move down the stack to offer execution (e.g. trading) of tokens but have yet to fully lean into offering custom, proprietary trading experiences.

The exception is Telegram, which has successfully integrated the social-financial experience. Still, Telegram’s UX is limited, and while degens have opted for it for convenience, there is room in the market for more Robinhood-esque experiences that offer seamless trading UX, easy onboarding, and retail-friendly features like commission-free trading. Moreover, new primitives like Farcaster frames and casts and Lens open actions further enable new types of financial transactions within these discovery-first networks.

Final Thoughts: Be Opinionated

Builders can create compelling social-financial games and networks by taking a unique approach to how app monetization and financialization impact their apps. The exchange-first approach is easier since it doesn’t necessarily rely on creating new consumer behaviors; people already want to trade attention. But a discovery-first approach where a platform controls eyes is historically more defensible than one that only controls orders (e.g. transactions). The primary goal of the discovery- or social-first approach is to iterate quickly, testing new consumer behaviors and social-financial dynamics until users showcase their revealed preferences that have the potential to grow into large social networks. I’m confident that the most successful apps will have opinionated, vertically integrated designs that create liquid marketplaces for new types of assets or marketplaces that otherwise catalyze new consumer behaviors.

+++

This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated.

Variant is an investor in Farcaster and Lens.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.