Towards Dedicated Model Foundries

“In this Grand Alliance, the combined R&D spending of TSMC and its ten biggest customers exceeds that of Samsung and Intel together.”

– Morris Chang, Founder of TSMC

Morris Chang was long obsessed with the idea of creating a dedicated chip foundry. Up until the 1990s, chip design and manufacturing were bundled together. Innovation was stifled as a result: manufacture and design are entirely different skill sets. And bundling them together limits competition as manufacturing is sufficiently complex and expensive to do well.

If only there was a dedicated foundry, rather than one rolled up into an entity with a broader mandate. Morris prophesied that a new wave of fab-less chip designers with IP of their own would emerge, over time creating even more demand for manufacturing than what already existed. A dedicated foundry would have competitive advantages over a company that covered more surface area. Firstly, by being focused on manufacturing alone, they could be a neutral (non-competitive) party to their customers. And secondly, by aggregating demand across chip designers, the dedicated foundry could become defensible: establishing economies of scale through amortizing expensive factory buildouts, and process power from hoarding talent and expertise.

Wants, Needs, and Incentives

But what does this have to do with AI models?

Today model architecture, pre-training and post-training are tightly bundled into a single entity. But each takes different strengths to get right.

The quality of:

- A model’s architecture is a function of a company’s AI talent and expertise.

- Pre-training is a function of the capital available to spend on compute to process massive amounts of data.

- Post-training is a function of having access to experts, evals and workflows that can inform the model’s performance on economically valuable tasks.

The well-funded, incumbent frontier labs, primarily spike on 1) and 2). Their strategies revolve around hoarding AI talent and compute through deploying vast amounts of capital. But they fall flat on their access to 3), which is mostly pent up in the companies deploying (not building) AI. It’s often their users (the deployers) who have a tight pulse on what’s needed to turn raw intelligence into economically valuable outcomes. But in spite of this, or perhaps in light of this, frontier labs have trudged forward in trying to compete on increasingly vertical services (e.g., agentic IDEs).

To overcome the discrepancy, frontier labs have deployed strategies to internalize domain and professional expertise. For example, in spending massive amounts on hourly wages to expert marketplaces like Mercor, and forward deploying engineers into customer companies to develop evals and insights on workflows. But paying experts is costly and SLAs prohibit direct deployment data from making its way back into the post-training process.

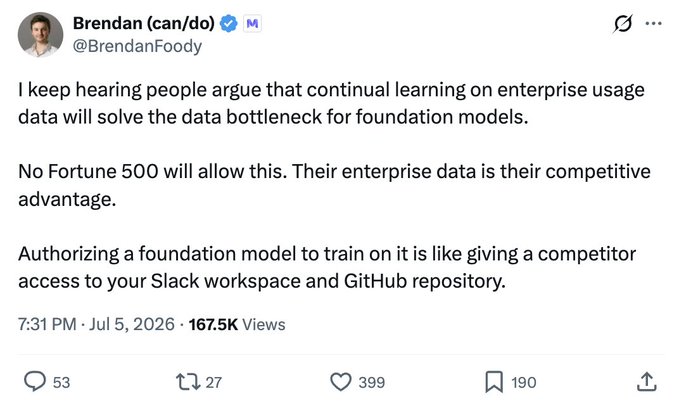

These bottlenecks were recently emphasized in a tweet from Mercor’s founder, Brendan Foody. In it he argues that continual learning will continue to be bottlenecked by a lack of enterprise data since no Fortune 500 will give up their enterprise data (competitive advantage) to a competitor.

But while this is a real concern within the current paradigm, there’s also an opportunity to overcome it through unbundling frontier labs and making Ownership a core tenet in the value proposition offered to customers.

Dedicated Model Foundries

In an idealized world, enterprises would train and own the models they use, unlocking two advantages in post-training over frontier labs:

- Expert data is subsidized by productive deployment rather than being a loss-leading initiative. Whereas today, experts are paid through marketplaces to simulate productive deployment, they would be hired to do the actual job and make money alongside the data they produce. Through subsidizing data acquisition with revenue from deployment, enterprises will have an advantage in post-training over isolated labs.

- There are no prohibitive SLAs. Any proprietary data can be directly used in the post-training. This contrasts the existing relationship between frontier labs and their customers, where only the understanding of FDEs can be integrated into the training process through newly-designed evals and workflows.

But in reality, enterprises still can’t afford the AI talent, capital and compute needed to design and train frontier foundation models. Herein lies a potential solution: Dedicated Model Foundries.

Dedicated model foundries, similar to chip foundries, would act as a neutral party. They would only own IP related to the training process, pre-trained foundation model, and perhaps optional hosting services. Rather than competing with enterprises on increasingly vertical products, they would exclusively license post-trained models to the enterprises which provided the proprietary data. In doing so, weights trained on proprietary data are only available to the enterprises which produced it. No longer constrained by having to choose between the risk of leaking proprietary advantages, and constraining model performance, companies will flock to participate.

There are already signs of this in the market. Today, companies like Applied Compute, Thinking Machines, and Prime Intellect post-train open-source models as a service. Unlike Anthropic or OpenAI, they don’t compete with their customers on developing models that may supplant them (as was the case with Cursor vs. Claude Code and Codex), they remain neutral instead.

This is a classic counterposition. Rather than employing the business model of selling tokens, Dedicated Model Foundries sell models. Rather than verticalizing to capture more of the deployment process, Dedicated Model Foundries commit to staying in their lane in order to align incentives with their customers. And while it’s possible for the incumbents to alter their business strategy and model, doing so would require significant effort, which leaves space for a challenger to make an aggressive move in the interim.

But what they gain in incentive alignment, they lose in a moat. If they don’t own the end models, or post-training data, they can’t establish the same compounding data advantages that vertical and frontier AI companies do.

So where could the moat come from?

After aggregating demand, dedicated model foundries may become better positioned to build the next wave frontier foundation models than incumbents. Open source is not necessarily the end-state for these companies, it might just be the bootstrapping mechanism. If the pre-trained foundation models remain proprietary, Dedicated Model Foundries will have the similar moats to that of the incumbents: scale economies in compute and process power from hoarding talent. Morris Chang was well aware of how the advantages of aggregating demand materialized for chips: “In this Grand Alliance, the combined R&D spending of TSMC and its ten biggest customers exceeds that of Samsung and Intel together.”

A Summary of Similar Strategies

If we were to summarize TSMC’s strategy as a dedicated chip foundry, it’d look roughly as follows:

- Unbundle chip manufacturing from design

- Expand the market of chip designers

- Align incentives and counterposition by not competing with designers

- Aggregate demand from chip designers

- Pour the proceeds from that demand into improving the manufacturing process

- Establish scale economies and process power

Not much changes when we map out the strategy for “dedicated model foundries”:

- Unbundle model training and data and model ownership

- Expand the market of model developers

- Align incentives and counterposition by not competing with model developers

- Aggregate demand from model developers

- Pour the proceeds from that demand into improving the training process

- Establish scale economies (on pre-training compute) and process power (across all training)

Let’s Connect!

There are still a handful of open questions on my mind regarding this thesis. To name a few:

- How much enterprise demand needs to be aggregated to overcome the billions of dollars in CapEx gaps between challengers and today’s frontier labs? Is this even feasible?

- How does the tradeoff space between in-context and in-weights learning affect this thesis? For example, if in-context learning is sufficient for incorporating proprietary know-how into AI workflows for the vast majority of scenarios, selling tokens, rather than custom, post-trained models may be sufficient as well.

- What does standardization look like for Post-Training-as-a-Service? Can it even become sufficiently standardized as we’ve seen play out in chip design?

- Can or will enterprise headcount evolve around the talent needed to push more post-training responsibility to the edges?

- Can weights remain open if “dedicated model foundries” monetize proprietary hosted services around post-training? Or do the weights need to also be proprietary for the business to be defensible?

If you have thoughts on these, or are building with similar ideas in mind, let’s connect!

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.