How DEXs Are Demonstrating Their Resilience

While DEX dollar-volume is down in this bear market, active usage is up.

Amid the meltdowns and tumult of the ongoing bear market, decentralized exchanges have thrived. DEXs have continued to operate as designed—and have even managed to capitalize on the prevailing volatility.

In this post, I take a look at the continuous growth of spot DEX usage and use onchain data to examine the driving factors behind their staying power and growing importance.

DEX usage has steadily grown

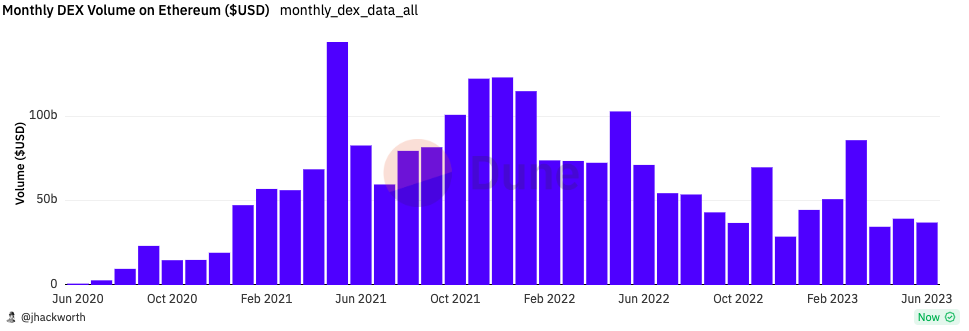

While decentralized exchanges date back to 2014, 2020’s “DeFi Summer” marked a pivotal moment. DeFi tokens mooned and DEX metrics soared, experiencing a compounded monthly growth rate of 47% in monthly volume and 26.4% in active users from June 2020 to June 2021.[1]

Source: Dune

As everyone in crypto is well aware, the party eventually stopped. After hitting its second-largest month ever in December 2021 at ~$123 billion, monthly DEX volume crashed to a bottom almost one year later of ~$28 billion.[2]

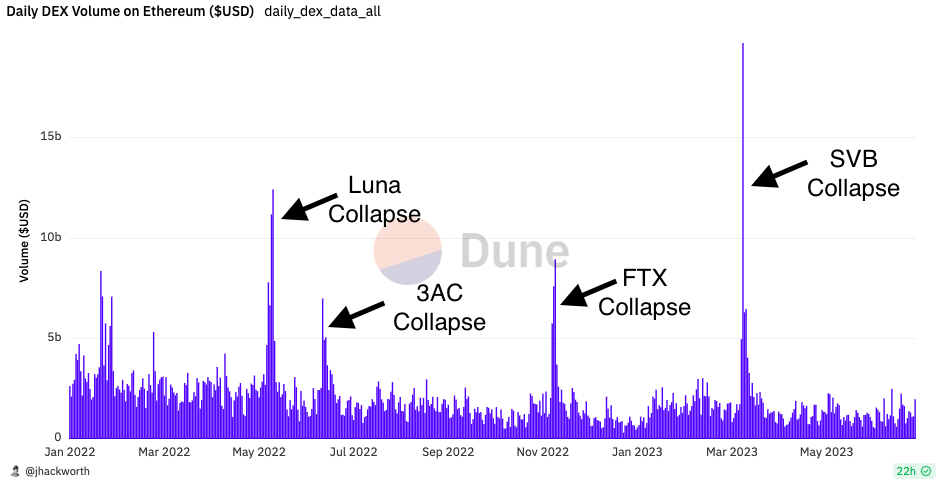

Despite the drop, DEXs continued to do exactly what they were programmed to do: provide permissionless trading. In fact, on days when centralized entities (like FTX, BlockFi, Celsius, and Voyager) were collapsing, DEXs saw large spikes in trading volume and some of their biggest single trading days ever. The SVB collapse (and USDC depeg) caused the largest single day of DEX trading volume with ~$19.7B in trading volume.[3]

Source: Dune

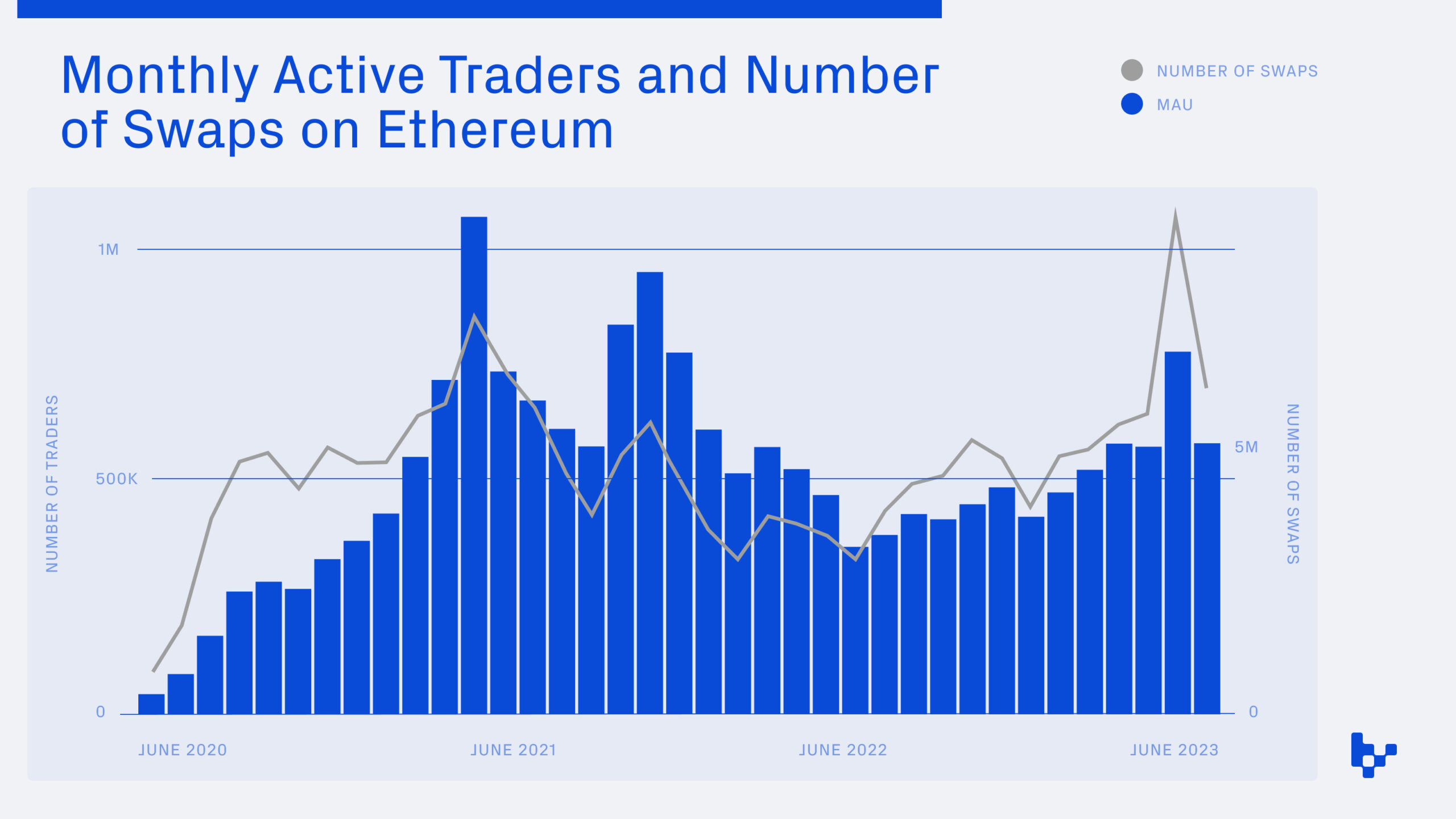

2023 has reversed the downward trend in volume: DEX volume on Ethereum saw an increase for the first three months, hitting a peak for the year in March at ~$85B.[2]

Volume has since decreased, but there are other indicators that DEX activity is on the rise. Fueled by new token launches, liquid staking tokens, and memecoins, active users and number of swaps have grown month over month an average of 11.7% and 7%, respectively, from December 2022 to June 2023.[4]

Source: Dune

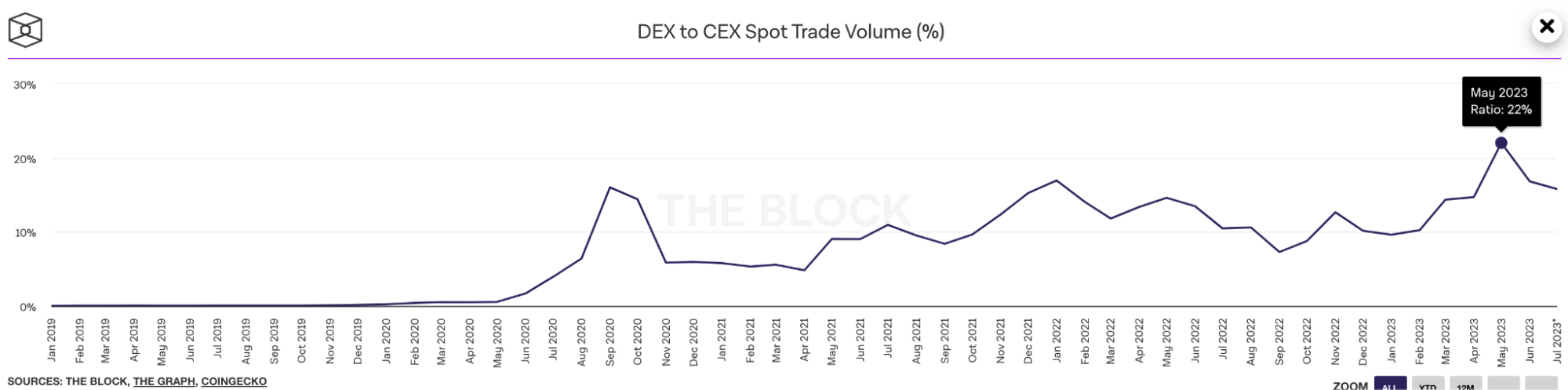

Another positive indicator is the increase in DEX to CEX spot volume. According to research from The Block, that ratio rose to 22% in May, the highest in history.[5]

Source: The Block

So, why the sudden rise in DEX to CEX spot volume, active users, and swaps? Many might point to the memecoin madness seen this past May. While that is certainly a large determining factor, it’s just one piece of a larger trend gaining steam.

What DEXs (AMMs in particular) are good at is providing liquidity for long-tail tokens (smaller-cap tokens such as memecoins) permissionlessly. Many tokens cannot be listed on centralized exchanges due to insufficient liquidity, regulatory concerns, or other factors. With DEXs, projects can instantly bootstrap liquidity, allowing for the greater market to participate. For many in crypto, their first onchain experience was swapping a token on a DEX because it wasn’t tradeable on a CEX. According to CoinGecko, Uniswap has almost 20 times more tokens listed than Coinbase and 3.4 times more than Binance.

| Exchange | # of Token Pairs Tracked on CoinGecko |

|---|---|

| Uniswap V2 (Ethereum) |

2967 |

| Uniswap V3 (Ethereum) | 1756 |

| Sushiswap (Ethereum) | 510 |

| Curve (Ethereum) | 97 |

| Coinbase | 241 |

| Binance | 1387 |

Source: CoinGecko Token Pairs on 7/25

Right now, much of the volume may be in memecoins, but in a future where there are millions of tokens, DEXs grant anyone the opportunity to find liquidity in their preferred assets. As more users become comfortable with DEXs—and increased regulatory scrutiny hits centralized exchanges—this upward trend will likely continue.

Uniswap extends its reach

It is clear that decentralized exchanges have found product-market fit in crypto, so who exactly is benefiting the most from increased adoption of decentralized spot exchanges?

The market leader for the moment is Uniswap, and data shows that there isn’t really one competitor close on its heels. Year to date, Uniswap has accounted for ~56% of total DEX volume across all chains, with its closest competitor Curve grabbing just 12% of the market share.[6]

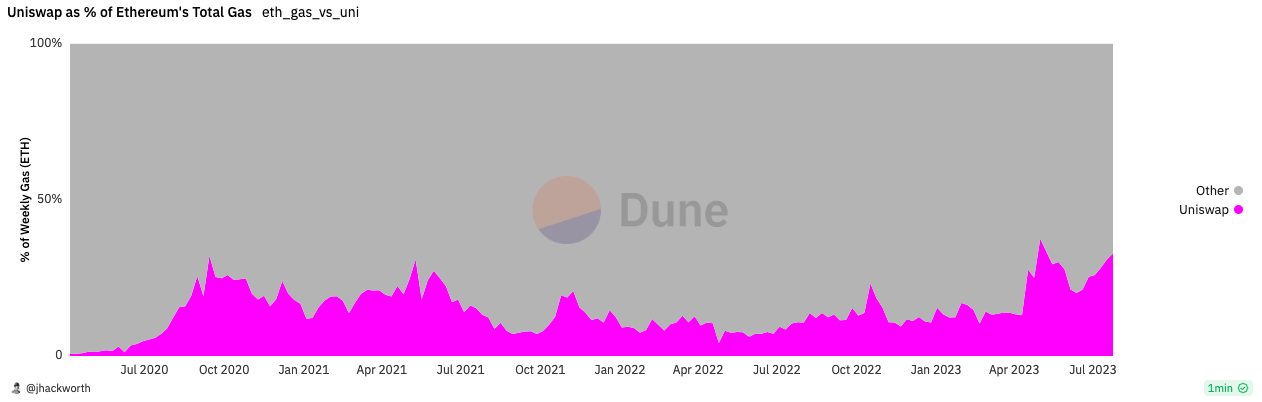

The demand for Uniswap may be highlighted by the amount of gas it consumes on Ethereum. Over the past year, 19% of Ethereum’s gas was due to Uniswap. This was ~4.5 larger than the next biggest set of contracts (Tether).[7]

Source: Dune

While Uniswap is one of the largest incumbents in DeFi, its biggest competition may prove not to be other DEXs, but centralized exchanges and traditional finance. In this much larger competitive field, Uniswap remains an underdog:

- For Q1 2023, Robinhood had 11.8M monthly users[8] and Coinbase had 8.4M.[9] By comparison, Uniswap only had 1.92M unique addresses complete a swap across all chains during that same period.[10]

- Coinbase processed over $145 billion in Q1 of 2023.[11] Uniswap did an estimated $154 billion in that period across all chains.[12] While this is an impressive stat for Uniswap, Binance completed over $1.9 trillion in spot volume,[11] which gives you a sense of how much bigger the largest CEX is than the largest DEX.

- On June 30, the Nasdaq saw ~$109.6 billion in trading volume[12] in the United States, which was 48x bigger than Uniswap’s total volume on that same day.[13]

(Note: I had to handpick some of these metrics from what was available in 10-K filings reports. If only there were a place where financial data were reported more often than quarterly!)

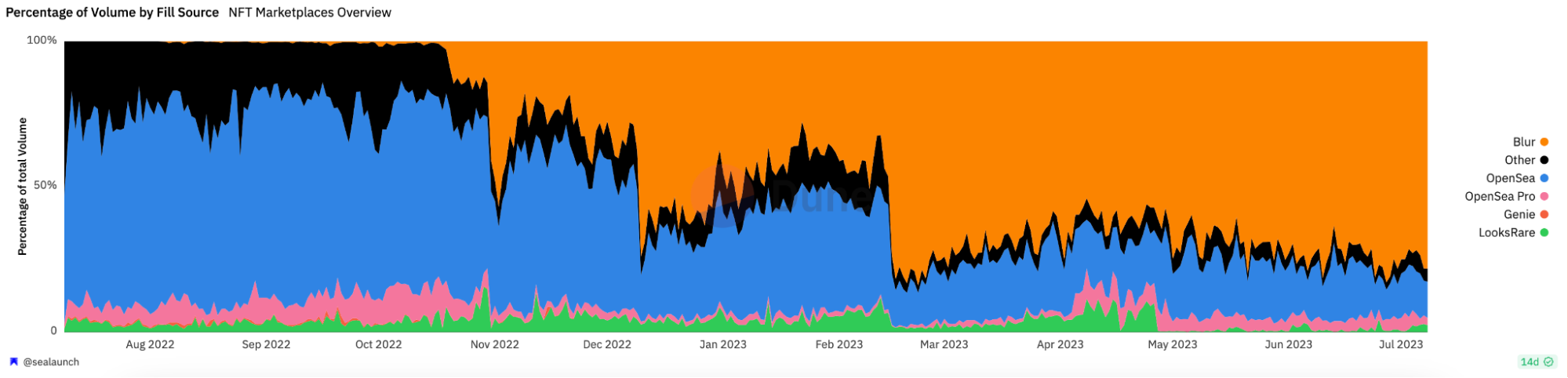

Blur as competitive case study for DEXs

As any history book can teach you, holding on to an empire is difficult. In crypto it is even more difficult. Nobody expected that a new marketplace could quickly challenge OpenSea’s dominance in NFT trading, but Blur did just that.

Source: Dune, SeaLaunch

One of the key ways Blur pulled this off was by attracting enhanced liquidity as well as “power users” to the network. It’s the same story for decentralized exchanges. Power users (usually institutional investors) will trade wherever the greatest liquidity (or token incentives) are.

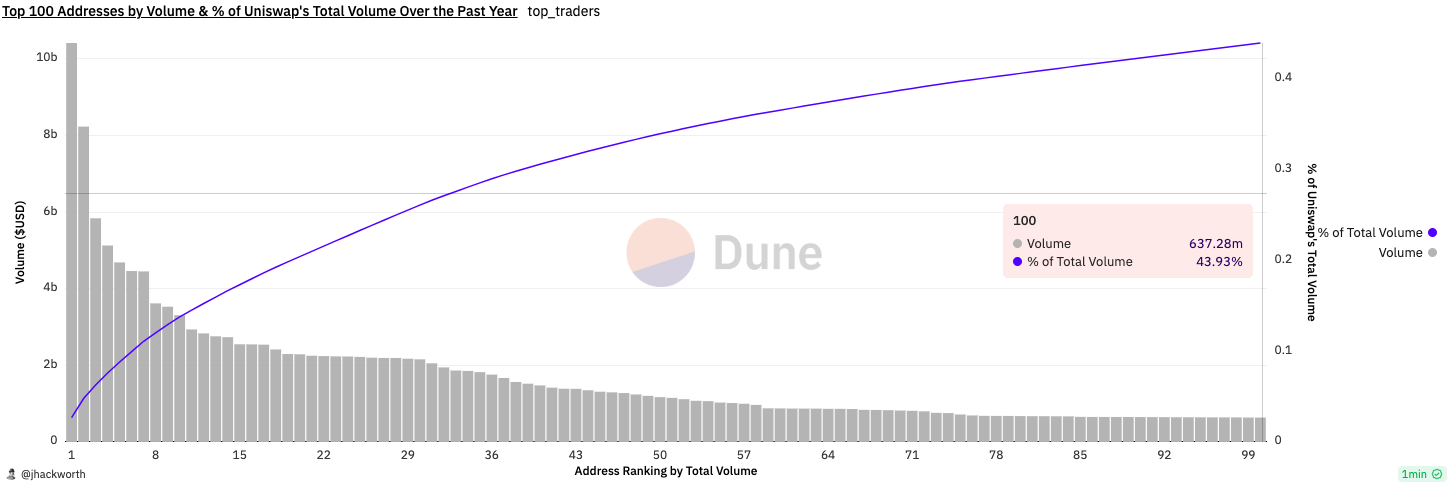

For Uniswap, the top 100 addresses by volume make up 44% of the DEX’s total volume in the past year.[14] If another exchange were to successfully tempt these users away with incentives, the protocol could quickly lose half of its trading volume. Uniswap must continue to innovate in order to attract liquidity and offer the best prices.

Source: Dune

The recent announcements of Uniswap V4 and UniswapX could help retain and attract new users by offering greater liquidity and enhanced customization.

Despite market turmoil, DEXs have functioned smoothly and continue to make the case for why decentralized finance works. One could even say that DEXs have the best product-market fit in all of crypto right now.

—

[1] Data Sourced from Dune, Calculation

[2] Data Sourced from Dune, Query

[3 Dune, March 11th Volume

[4] Data Sourced from Dune, Calculation

[5] The Block, DEX to CEX Spot Trade Volume

[6] Token Terminal, DEX Market Share

[7] Dune, Query to Calculate Ethereum Gas Usage

[8] Robinhood, Q1 Press Release

[9] The Block, Coinbase Monthly Transacting Users

[10] Dune, Uniswap Q1 2023 Stats

[11] The Block, Crypto Monthly Spot Exchange Volume

[12] US Equity Total, NASDAQ Trader

[13] Dune, Uniswap Volume on June 30th 2023

[14] Dune, Query on Top 100 Addresses

+++

Variant is an investor in Uniswap. This post is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.