Daniel Barabander

Investing in Derive

We’re excited to announce our investment in Derive, the leading onchain options exchange, because we believe the market is underestimating options, this team, and their product.

The case for onchain options only makes sense if you believe crypto can serve as real financial infrastructure. If crypto were only about short-term, high-leverage speculation, perps would be all we need. They’re simple, intuitive, and concentrate liquidity into a single market per asset. In early crypto — with thin liquidity, long-tail assets, and fragile infrastructure — that prioritization made sense. UX mattered more than financial expressiveness

But as the market matures, perps alone are proving to be insufficient for leveraged trading. Funding rates are uncertain: you can be non-consensus and right early on, but if the market ends up agreeing, you have to pay the price. And liquidations permanently wipe out positions from brief volatility even if they end up being right. This came to a head when perps traders were mass liquidated on October 10, demonstrating the risks of flash crashes to perp positions.

Options offer a solution: you pay a one-time cost upfront to get liquidation-free leverage. Outcomes are path-independent — what matters is whether the thesis is correct, not whether the market briefly moves against you along the way. This makes options fundamentally better suited for longer-term, leveraged positions.

At the same time, another catalyst is emerging: “Yieldmaggedon.” The era of free yield via airdrop farming, incentives, and ponzinomics is ending. As yields compress, capital has chased opaque strategies that disguise risk as easy excess return. The market is relearning a basic truth: higher yield means higher risk.

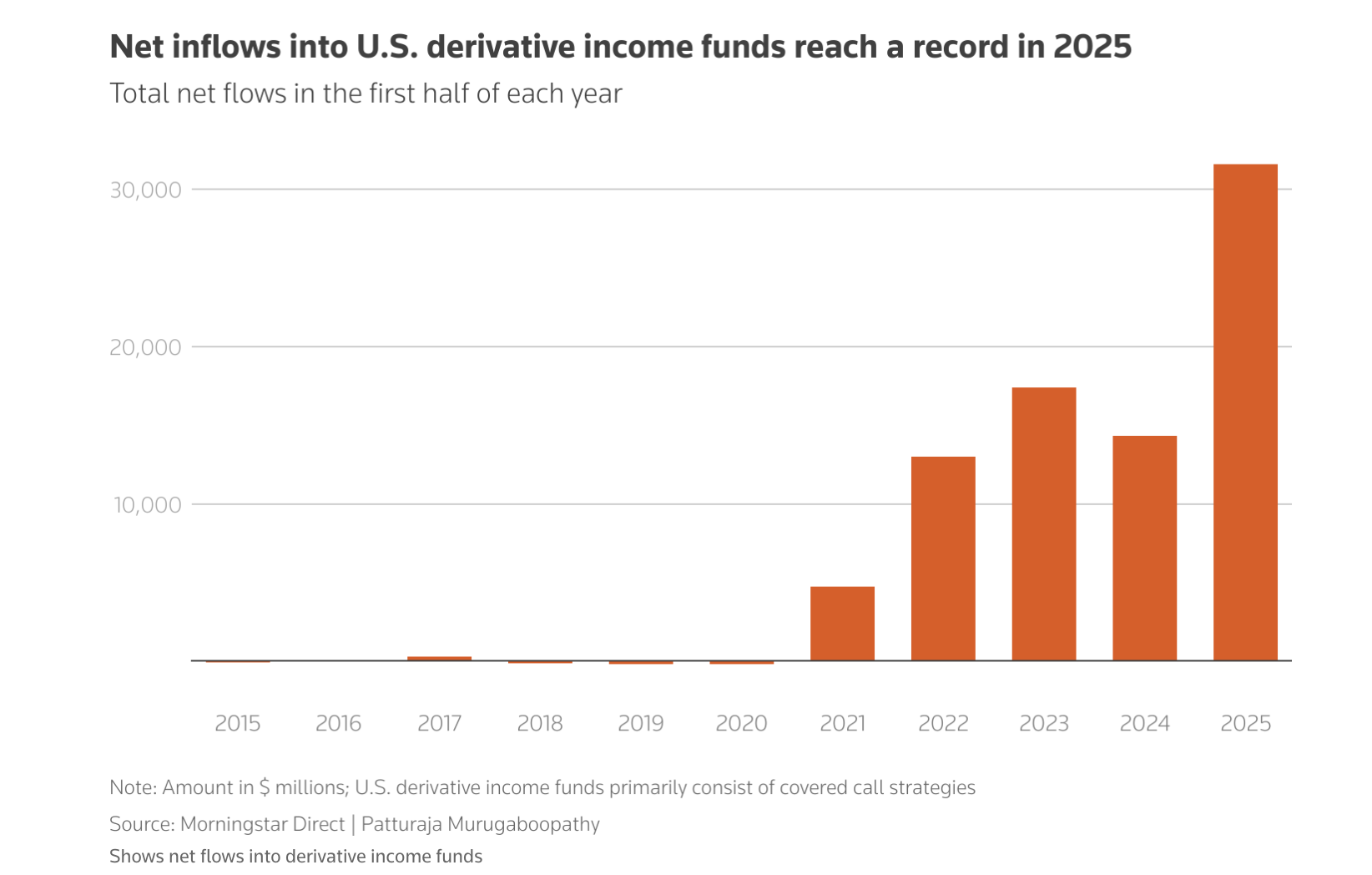

As an alternative, options provide a path to earn yield by taking transparent risks. Options-selling strategies involve known strikes, known expirations, observable volatility, and known upfront cash flows, instead of black boxes and hoping nothing breaks. Traditional finance has known this for a long time, and is now seeing a new wave of growth on the back of making options strategies more accessible — derivative-income ETFs (which primarily consist of managed call strategies) are rapidly growing, with over ~$145b in AUM and over $30b in inflows in the first half of 2025. It stands to reason that crypto will undergo a similar shift, with options-based strategies emerging as a primary way to earn yield through transparent, well-defined risk.

Options also unlock entire classes of trades that perps simply cannot support: volatility trading, structured products, defined-downside strategies, and interest-rate hedging. Many financial expressions are not “perpifiable,” so other instruments (like options) will always be needed.

While the adoption of options in crypto hasn’t seen the explosive growth of perps, that is not only unsurprising but expected. In every financial setting, options emerge only after spot and futures liquidity deepen, market participants sophisticate, and the infrastructure needed to hedge non-linear exposures comes online. Crypto is now approaching that inflection point.

Onchain is the natural end state for all options activity, not just crypto. Options markets become open, verifiable, and programmable onchain. Positions can be tokenized, recombined, and embedded into new products without contracting costs or operational friction. This is more powerful than what’s feasible in offchain finance.

So the real question wasn’t whether onchain options are coming — it is who could actually make them work at scale.

As we dug deeper, we kept hearing the same thing: “You have to meet Nick and the rest of the Derive team.” It quickly became apparent to us why. They are true experts, pulling from years of experience at SIG, Deribit, Tradeweb, and Paradigm. Using their experience, they’ve built a sophisticated onchain options exchange, hosting an advanced margin system, collateral flexibility, structured product RFQs, and a central limit orderbook. This took a long time to get right, but the team’s doggedness is starting to pay dividends. Industry-leading market makers are onboarding, unique sources of taker flow are following suit, and third-party applications are building on top. The exchange crossed $20B in inception-to-date trading volume just last week. As trading terminals, structured product builders, and asset managers look for places to deploy, the Derive platform and team will be the natural schelling point.

This isn’t the easiest market to build in, which is precisely why it matters.

So given the option, we needed to buy a call on their journey.

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.