Onchain Options, Why Now?

If you’ve been following my posts, you’ve probably noticed I’ve been talking a lot about onchain options and the traction Derive has been seeing. The most common response I’ve gotten from investors and users is that onchain options have been tried… and failed time and time again.

Many people I’ve spoken to already understand where perps are incomplete. Funding rate uncertainty and strictly linear payoffs are two obvious constraints that options don’t have. But opponents to onchain options argue that users don’t care. They claim that onchain users aren’t looking for certain costs or complex payoffs — “they just want to gamble”.

But there are a handful of reasons to rethink the orthodox position. A perfect storm for adoption is brewing:

- Infrastructure advancements

Ribbon, Dopex, and other options vaults had a moment in 2021-2022 but failed to retain traction. Their protocols were heavily reliant on external oracles and sluggish infrastructure (built on Ethereum mainnet).

Fast forward to 2026, and several critical advancements have materialized. Hyperliquid could never have been built as a smart contract on Ethereum or with an overreliance on external oracles. It needed a highly performant, application-specific environment in order to host price discovery with deep, active market-making on an orderbook.

- The growth of exchange-traded options offchain

Options have been used for quite a while in crypto. However, much of the flows were concentrated in OTC markets, where things move at lower frequencies and are less automated. This limited the number of players that could reasonably participate. Rather than it being a competition across trading desks on who can offer the best pricing, OTC desks rely heavily on reputation and sales capacity to win flow.

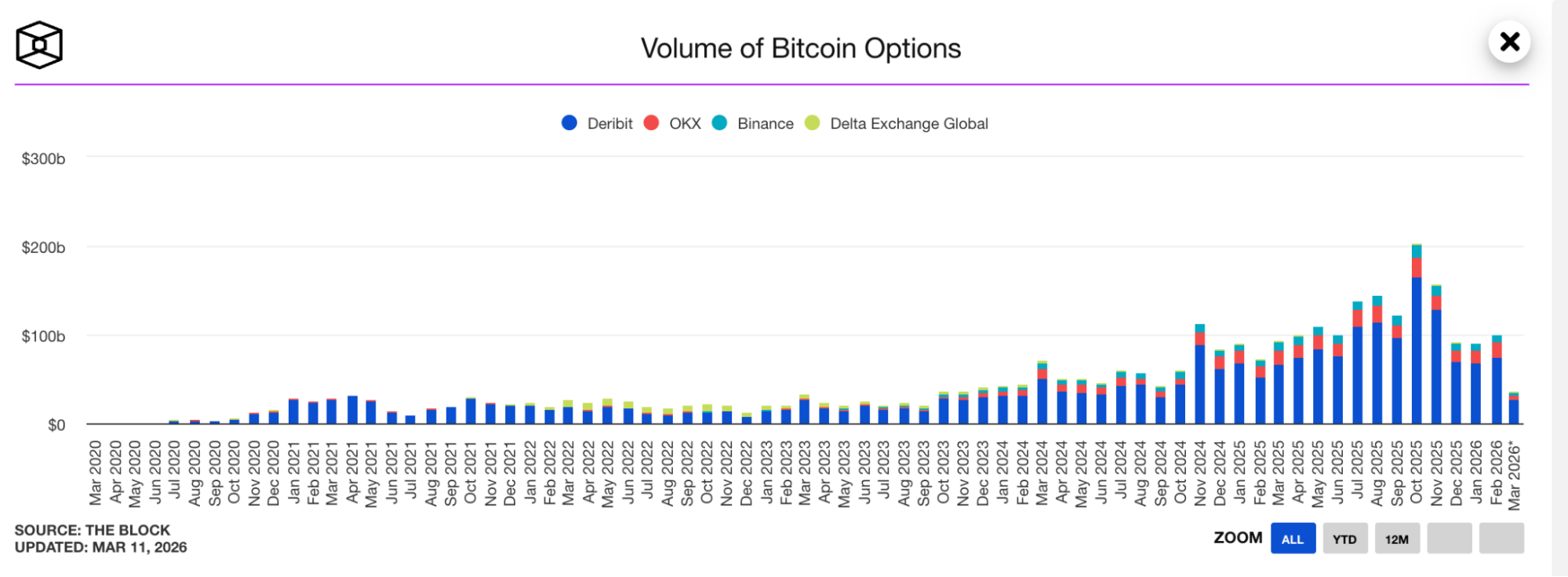

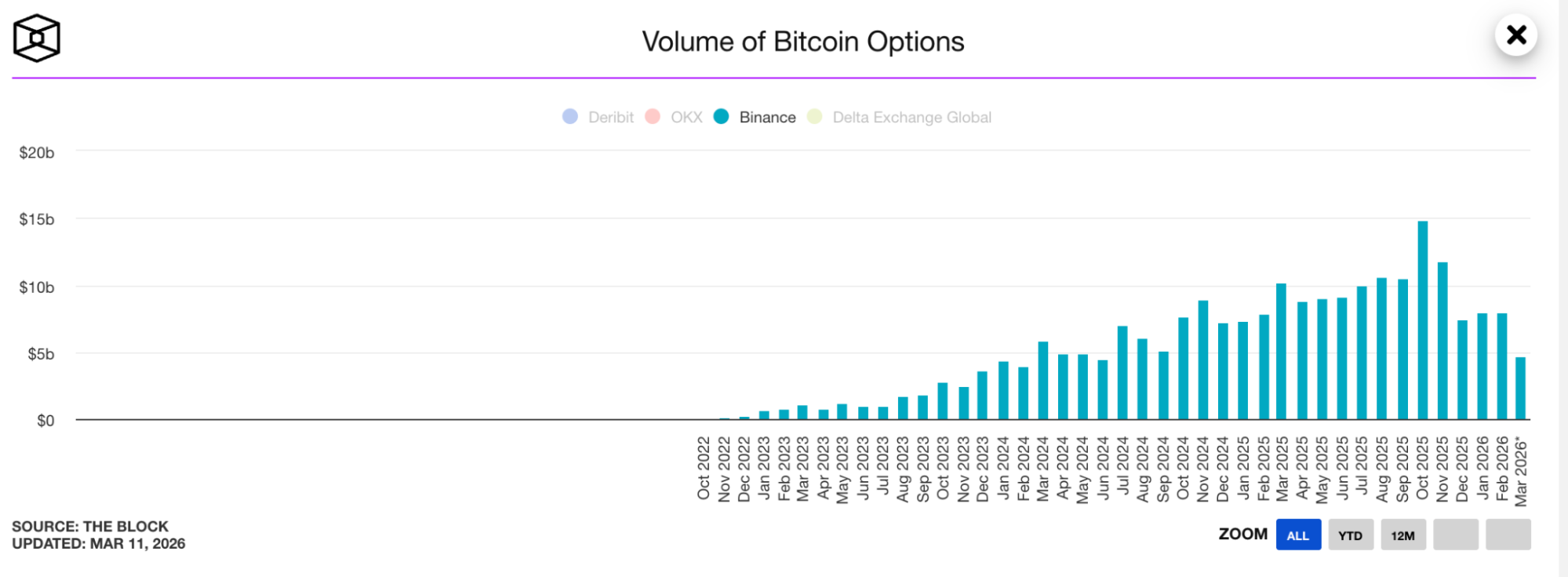

Deribit was founded in 2016, but it wasn’t until 2021 that it started to see real traction. By successfully moving a meaningful portion of the existing OTC market onto its exchange, it enabled a much longer tail of options desks to emerge.

Offchain exchange-traded venues made open competition possible. And it also drove the existing players to build automated systems that operate at lower frequencies.

This is relevant for onchain exchanges because it lowers the barrier to entry. Instead of needing to convince makers to perform two tasks:

1) building systems for an exchange trading from scratch, and

2) integrating it within a novel, onchain environment

the offchain exchanges bootstrapping simplifies the task of onboarding makers to only the second.

- Coinbase’s Deribit acquisition

Coinbase’s acquisition of Deribit is notable for two reasons. The first is that it gives credence to the future growth of crypto options exchanges. The second is that a huge portion of Deribit’s activity is driven by ex-US users.

Unsurprisingly, crypto options are most liquid on the major stores of value: BTC and ETH. The core value proposition of these assets is that they are non-sovereign stores of wealth. It is reasonable to expect that many of the ex-US traders who hold exposure to non-sovereign stores of wealth are uncomfortable with their wealth being held in US-regulated institutions.

While onchain exchanges are one option for these users to migrate to, it’s not the only one. Binance, for example, has a fairly successful options market and significant distribution with ex-US users.

But one notable constraint for Binance is the degree to which bootstrapping an options market requires dedicated focus. Deribit won not because it was focused on becoming the largest exchange, but because it was hyper-focused on becoming the largest options exchange. The makers and takers that dominate the options market are not necessarily the same ones that dominate spot and perps markets. Creating a Schelling point for options-focused desks requires targeted business development where incentives are aligned with the right stakeholders.

But the question still remains: Why is there an opportunity for an onchain exchange rather than a new centralized exchange?

- The materialization of onchain’s value proposition

FTX’s collapse in 2022 was one of the strongest tailwinds for Hyperliquid’s success. Following the collapse, a ripple of insolvencies tore through the market, destroying trust in centralized exchanges and custodial desks.

Bootstrapping a new centralized venue requires bootstrapping a considerable degree of trust in a centralized intermediary, and FTX made this even more acute. Many traders became more comfortable with self-custodial venues where they can track their balances more effectively and worry less about hidden insolvencies.

The practical, average-case advantages of self-custody also became clearer. Trading firms that trade on multiple venues often need to rebalance. When doing so, they are transferring large sums of funds in and out in a time-sensitive manner. For example, when a hedge is losing value, it may need additional collateral to avoid liquidation. In these scenarios, a temporary account freeze or withdrawal/deposit delays can be the difference between reward and ruin. Onchain exchanges are less discretionary in nature and settle quickly. This reduces the risks associated with cross-venue rebalancing, saving traders headaches and money.

- Markets naturally mature from less to more complexity

In 1792, the NYSE was founded. The first step in standardizing spot trading in the U.S.

Half a century later, in 1848, the CBOT was founded. The first step in standardizing futures trading in the U.S.

And then, finally, over a century later, in 1973, the CBOE was founded. The first step in standardizing options trading in the U.S.

Basically a century between each. To understand why, look no further than how each is priced. The more moving pieces there are, the longer it takes for the market to understand how and why to use something.

Crypto CEXs speed-ran this evolution. First, spot trading took off with Mt. Gox. Next, perps trading took off on Bitmex. And, finally, only some time later did options take off on Deribit. Only a few years passed between each.

It should be expected that a similar thing will play out onchain.

- It’s not perps OR options, it’s perps AND options (the need to delta hedge)

Aside from complexity, there’s another reason why liquid futures markets precede liquid options markets: delta hedging.

Market makers aren’t in the business of taking directional bets; they are in the business of pricing assets. The more directional exposure a market maker takes on, the greater their risk. The greater their risk, the wider their quotes and the less liquid their markets will be.

To hedge their exposure, an options market maker must have some way to go long and short the underlying, ideally with leverage and cross-margining. This is where futures (or, in crypto’s case, perpetual futures) become a necessary component for liquid options markets.

- 10/10 liquidations and how perps are short-term derivatives

Perps have been the dominant form of leveraged crypto trading for both on and offchain markets. This is largely due to their simplicity. Instead of having a different market for each maturity and making users think about complex payoffs, perps aggregate liquidity into a single market per asset and have an easy-to-reason-about payoff.

But crypto is a volatile asset class. Markets can jump violently up or down in an instant. This played out on 10/10. When prices wicked downwards, longs got liquidated en masse, even though prices recovered shortly after.

The event highlighted a major flaw in perps. It doesn’t just matter if you’re right about the direction of price — it also matters what path is taken to get there. If price moves sufficiently against your position for even a moment, you can be liquidated.

This risk becomes particularly important when a trader is trying to express a longer-term view. And perps’ shortfalls for expressing longer-term views are exacerbated by uncertainty over funding costs, which increase over time.

Options under this lens counterposition against perps. You pay once upfront and have exposure until maturity regardless of the path price takes. This makes them attractive for expressing longer-term views with leverage.

With a recent event to remind traders of these advantages, it’s reasonable to expect we’ll see at least a marginal migration of traders becoming options buyers when their preference suits it.

- Yield compression, Stream Finance, and retail product-market fit in options selling

Up to this point, we’ve only identified reasons why sophisticated players are willing to trade options onchain. They care about performance and risk, two areas that onchain venues are now able to compete with (or even surpass) centralized venues on.

But where is retail in all of this?

Market makers love to service retail demand because they consider their orderflow to be uninformed. This builds market makers’ confidence that the trades they take will be profitable. As a result, exchanges that can onboard retail are better positioned to thrive. By establishing a honey pot for market makers, exchanges build up their liquidity, which attracts less price-sensitive sources of orderflow and establishes a network effect.

Opponents of onchain options typically make two connected claims:

1) the demographic of onchain users is largely retail, and

2) perps satisfy the vast majority of demand for retail trading already

I’ve already made a case for why 1) is changing. But there’s reason to strongly reject 2).

Retail traders are particularly risk-seeking. When it comes to yield, they’ve shown a willingness to hold large amounts of capital in risky strategies. But despite the demand, onchain yields have drastically compressed. Incentives, points farming, and basis trades are no longer reliable sources of easy, outsized returns. This is pushing users even further down the risk curve, where opaque risks are disguised as easy yield.

We saw this come to a head with the collapse of Stream Finance. Stream didn’t disclose the strategies it used to generate its advertised 18% APY on USDC. But what we came to find out was that it was essentially giving undercollateralized loans to various fund managers who had full discretion. When one fund manager decided to use the loan to plug holes in their balance sheet, Stream depositors were stuck paying the bill.

While you could write a whole series of posts about the nasty aftermath, that’s besides the point. What is relevant here is how options selling enables a middle ground.

Covered options selling strategies are, in essence, yield strategies. Traders can select the prices at which they’re willing to sell or buy an asset and receive some cash flow upfront in exchange for their willingness to do so. While this is not without risk (if price moves against them, they take on downside or lose upside), it is at least a transparent trade of risk for yield. And given the risk-seeking nature of onchain users, there’s reason to believe that many are willing to make that trade.

Rysk Finance TVL on DeFi Llama

Rysk Finance TVL on DeFi Llama

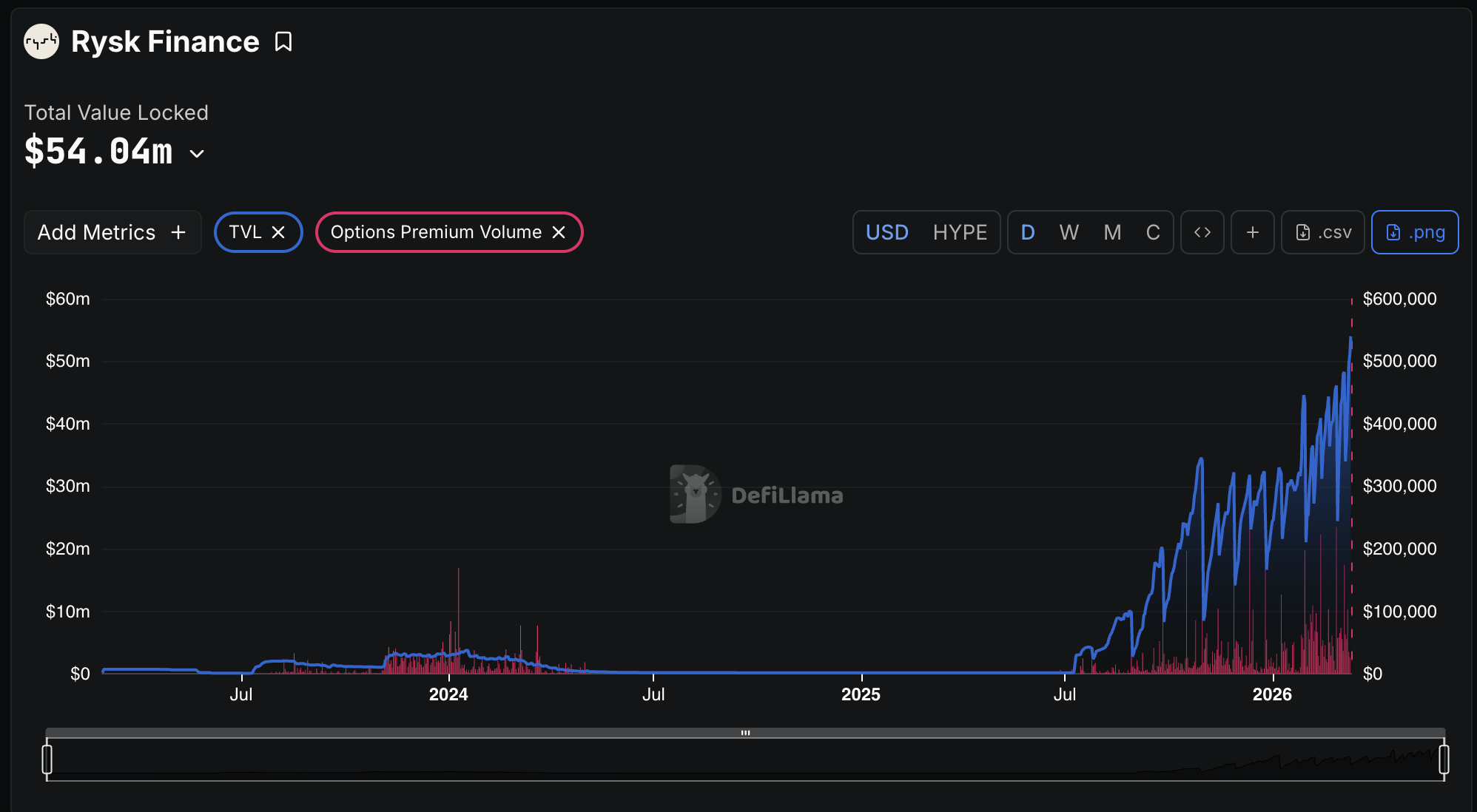

We’re starting to see this play out with the recent success of Rysk, a covered options-selling protocol. Despite having built its protocol over a series of years, it only started to see meaningful traction in July 2025. Its relaunch coincided with industry-wide yield compression and Stream Finance’s collapse, potentially giving it the tailwinds it needed to take off.

Options-selling strategies packaged as yield are not specific to onchain markets. “The wheel,” a popular strategy run by retail traders, even has a dedicated subreddit with over 10k monthly visitors. It’s referred to as a “triple income” strategy, which describes how its users sell puts for cash, buy the underlying on exercise, and then sell calls to earn more cash (and repeat the cycle).

Source : Swan Global

Source : Swan Global

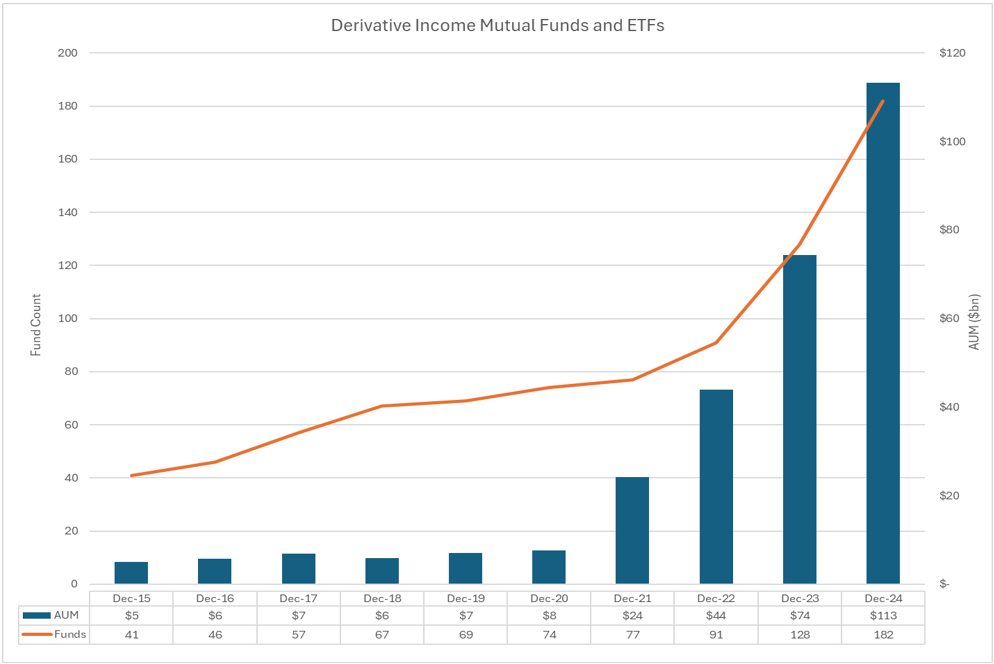

We’ve also seen a sharp rise in the AUM of derivative income mutual funds and ETFs (reaching >$100B in 2024). The vast majority of this growth is being driven by options-selling strategies, particularly covered call selling. They allow passive depositors to retain some exposure to the market while receiving regular cash flow from option sales.

- Euphoria, other experiments, and retail product-market fit in expressive trading

Options’ product market fit with retail won’t be exclusive to options-selling strategies. I firmly believe that options-buying will also find its place.

Many have pointed out that 0DTEs and perps target the same audiences: retail traders who want short-term, leveraged exposure. For this segment, perps are likely superior. With perps, there’s no need to think about convexity or choosing a strike price. These features simplify the act of entering a position. This is also why I find arguments for options adoption that cite Robinhood’s options volume and revenue as evidence for product-market fit misguided. Their current options business will likely be eaten up after launching perps.

But all is not lost. What options lose in simplicity, they make up for in their flexibility to create any imaginable payoff.

The best instantiation of this so far is Euphoria, a touch trading app.

The UX has two core features: a real-time price path and clickable cells that correspond to a price and time. Each cell has a payoff, and when you click it, you lock that payoff in. If the price path ends up hitting the cell, users receive a payout. Without needing to know it, Euphoria users will be trading binary option spreads.

The general thing to take away here is that the flexibility of options unlocks new trading experiences. And a great UX can mask any of the associated complexity. Euphoria is just the start.

The thing I’m most excited about is what happens when you combine this flexibility with open, programmable APIs. One of the unique features of onchain venues is their ability to support second-order innovation. Anyone can plug into existing sources of liquidity and compose. This vastly reduces the bootstrapping costs of a new trading experience. And only recently have onchain options exchanges become sufficiently liquid to make it worth a builder’s time.

- We’re already taking off

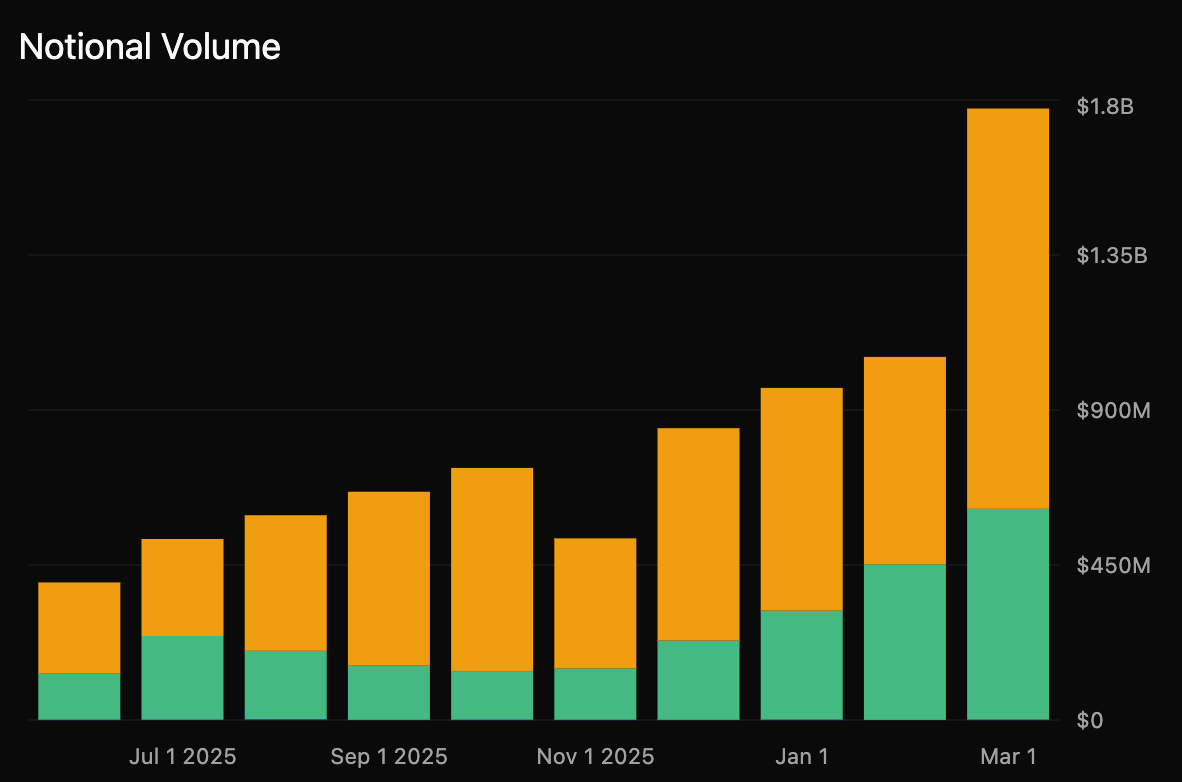

Derive, the largest onchain options exchange, has been on a tear in recent weeks.

Monthly notional volume on Derive

It’s built up significant liquidity, printing $100M+ notional trades, and attracting novel third-party apps. It became the third-largest onchain derivatives exchange by open interest, it has recently expanded to new markets like HYPE and SOL options, and volumes have been consistently growing.

- Money Legos and The Long Game

The future for onchain options could be much bigger than what Deribit or any other centralized exchange can create. As Nick from Derive puts it, it’s a global, programmable, 24/7 factory for any payoff on any asset.

The industry has long talked about “money legos”. Financial components that can be packaged together in different ways without the negotiation and formation costs of traditional contracts. In the limit, onchain finance can serve users the customizability of OTC with the liquidity and cost structure of trading on standardized exchanges. Within this limit the flexibility of options is uniquely suited to serve as a core building block, leading me to believe that the market could be much bigger than anyone expects.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.