Putting All Your Calls in One Basket

Paths Towards a Successful Onchain Options Market

If crypto’s core value proposition is to provide new financial rails, it is perplexing that onchain options have yet to take off.

In U.S. equities alone, single-stock options trade around $450 billion daily — roughly 0.7% of the $68 trillion U.S. equity market. By contrast, crypto options see about $2 billion in daily volume, which amounts to just 0.06% of crypto’s ~$3 trillion market cap (10x lower than equities on a relative basis). And while DEXs now shoulder upwards of 20% of crypto spot volume, nearly all options activity still runs through CEXs like Deribit.1

The disparity between traditional and onchain options markets stems from early designs, constrained by primitive infrastructure, that failed to satisfy the two ingredients of a healthy market: protecting liquidity providers from bad orderflow and attracting good orderflow.

Today, the infrastructure exists to solve the former — liquidity providers can finally avoid being picked off by arbitrageurs. The remaining challenge, and the focus of this piece, is the latter: identifying a go-to-market (GTM) strategy to attract good orderflow. We argue that onchain options protocols can thrive by targeting two distinct sources of good orderflow: hedgers and retail.

The Trials and Tribulations of Onchain Options

As was the case for spot markets, the first onchain options protocols pulled from the dominant market design in traditional finance — orderbooks.

In the early days of Ethereum, activity was sparse, making gas relatively cheap. Therefore, an orderbook seemed like a reasonable mechanism for options trading. Options orderbooks date back to at least March 2016 with EtherOpt. (EtherDelta, the first popular spot orderbook on Ethereum, came along a few months later.) But in practice, market making was difficult onchain. Gas fees and network latency made it expensive for market makers to provide good quotes and avoid taking bad trades.

To solve these issues, the next wave of options protocols used AMMs. Instead of relying on individuals to make the market, AMMs get the price from an internal token balance within a liquidity pool or from an external price oracle. In the former, the price updates when traders buy or sell tokens into the liquidity pool (changing the pool’s internal balances); the liquidity providers themselves don’t set the price. With the latter, prices are updated periodically when a new oracle price is published onchain. From 2019 to 2021, protocols like Opyn, Hegic, Dopex, and Ribbon all followed this path.

Unfortunately, AMM-based protocols did not dramatically boost onchain options adoption. The same property that makes AMMs gas efficient (i.e., traders or lagging oracle feeds setting the price instead of liquidity providers) leaves liquidity providers prone to losing value to arbitrageurs (aka adverse selection).

The thing that may have stunted adoption the most, however, is that all early iterations of options protocols (both orderbooks and AMM-based designs) required fully collateralized short positions. In other words, short calls had to be covered and short puts had to be cash-secured, making the protocols capital inefficient and removing a key source of leverage that retail desires. Without this leverage, when incentives dried up, little retail demand was left.

Sustainable Options Exchange: Attract Good Orderflow, Avoid Bad Orderflow

Let’s start with the basics. Healthy markets need two things:

- The ability for liquidity providers to avoid “bad orderflow” (aka not lose money unnecessarily). By “bad orderflow,” we mean arbitrageurs who are earning practically risk-free profits at the expense of liquidity providers.

- A strong source of demand to provide “good orderflow” (aka make money). By “good orderflow” we mean price-insensitive traders who earn profits for liquidity providers when they are charged a spread.

Our review of the history of onchain options protocols reveals they’ve failed in the past because neither of the above was satisfied:

- Limitations on technical infrastructure for early options protocols prevented liquidity providers from avoiding bad orderflow. The traditional way liquidity providers avoid bad orderflow is by updating quotes at no cost and at high frequencies on an orderbook, but the latency and fees on orderbook protocols in 2016 made this impossible to do onchain. Moving to AMMs did not solve this problem because the lazy pricing mechanisms disadvantage liquidity providers against arbitrageurs.

- The requirement of full collateralization removed a feature of options (leverage) desired by retail, which is a key source of good orderflow. Without any other ideas of how to use options onchain, there was no source of good orderflow.

Accordingly, if we want to build an onchain options protocol in 2025, we must ensure both pieces of the puzzle are solved for.

A lot has changed in recent years to suggest we can now build infrastructure that allows liquidity providers to avoid bad orderflow. The rise in application- (or sector-) specific infrastructure has significantly improved market design for liquidity providers across a variety of financial applications. At the top of this list are things like speed bumps (which delay taker orders); sequencing priority for post-only; cancel orders and price oracle updates; little-to-no gas costs; and mechanisms for censorship-resistant inclusion at high frequencies (like multiple-concurrent leaders).

With scaling innovations, we also can now build applications that good orderflow desires. For example, improvements in consensus design and ZK have led to cheap-enough blockspace for implementing sophisticated margin engines onchain, which obviate the need for full collateralization.

Solving the bad orderflow issue is largely a technical question and is, in many senses, the “easier” issue. Yes, building this infrastructure is technically complex, but that is not the moat. And even though new infrastructure can enable a protocol that attracts good overflow, that does not mean good orderflow will just magically appear. Rather, the core question, and the focus of this piece, is as follows: Assuming we now have the infrastructure to support good orderflow, what kind of GTM should projects target to attract this demand? If we can answer this, we have a fighting chance at building a sustainable onchain options protocol.

Profiles of Price-Insensitive Demand (Good Orderflow)

As discussed above, good orderflow is price-insensitive demand. In general, two core profiles make up price-insensitive demand for options: (1) hedgers and (2) retail. Each profile has different objectives and therefore utilizes options differently.

Hedgers

By hedgers, we mean institutions or operating businesses for whom reducing risk is valuable enough to justify paying some amount above market value.

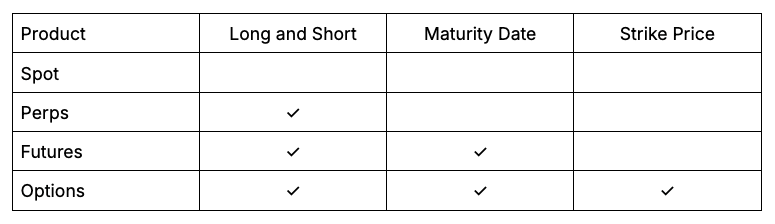

Options are attractive to hedgers because they allow them to cap downside risk with precision by choosing the exact price level (the strike) at which they stop taking losses. This differs from futures, which hedge in an all-or-nothing way; futures protect your position in all scenarios, but don’t let you express at what price that protection should begin.

Hedgers make up the vast majority of current demand for crypto options, and we expect this to mainly come from miners who represent the first batch of “onchain institutions.” This can be seen in the fact that BTC and ETH dominate options volume and mining/validating on these chains is significantly more institutionalized than others. Hedging is important to miners because their revenues are denominated in volatile crypto assets, while many of their obligations — such as payroll, hardware, hosting, etc. — are denominated in fiat.

Retail

By retail, we mean individual speculators who are financially motivated but relatively unsophisticated — they often trade based on emotion, conviction, or narrative rather than models and algorithms. They generally want simple UX for trading, and their demand is driven by getting wealthy quickly rather than being disciplined about risk and reward.

As discussed above, the reason why retail has historically been attracted to options is leverage. This is evidenced by the explosion in popularity of zero-day options (0DTEs) in tradfi retail — 0DTEs are largely seen as a speculative leveraged trading vehicle. In May 2025, 0DTEs accounted for more than 61% of S&P 500 options volume, and it is believed most of this volume comes from retail users (particularly on Robinhood).

Despite their popularity in tradfi, retail adoption of options in crypto is effectively zero. This is because there is even a better crypto instrument for retail to go long/short with leverage that’s not currently available in tradfi: perps.

As we saw with hedging, options’ superpower is their granularity. An options trader can consider long/short, time, and strike, making options much more versatile than spot, perps, or futures trades.

While more components creates more granularity, which is desired by the hedger, it also requires more decisions, which is generally overwhelming for retail. In fact, 0DTEs’ success in tradfi retail can largely be explained by the fact that 0DTEs improve options’ UX problem by removing (or dramatically simplifying) the time dimension (“zero day”) to provide a simple instrument to go long or short with leverage.

The reason why options aren’t viewed as a leverage proposition in crypto is because perps are already incredibly popular and represent an even simpler instrument than the 0DTE to go long/short with leverage. They remove both the time and strike price dimensions from the equation so users can go perpetually long/short with leverage. That is, perps achieve the same objective (leverage for retail) as options with simpler UX. Therefore, the value-add of options is severely diminished.

However, all is not lost for options and crypto retail. Besides simple ways to go long/short with leverage, retail also desires fun and novel trading experiences. Options’ granularity means they can enable new trading experiences. One particularly powerful feature is allowing participants to take a position on volatility itself. Take the popularity of the Bitcoin Volatility Index (BVOL) offered by FTX (before going defunct). BVOL tokenized exposure to implied volatility, letting traders bet directly on how much Bitcoin’s price would move (regardless of direction) without managing complex options positions. It packaged what would normally require straddles or strangles into a single, tradable token, making volatility speculation simple and accessible for retail users.

GTMs for Price-Insensitive Demand (Good Orderflow)

Now that we’ve identified the profiles of price-insensitive demand, let’s describe GTM strategies protocols can use to target each profile to attract good orderflow to an onchain options protocol.

Hedgers GTM: Meet Miners Where They Are

We believe the best GTM strategy to capture hedging flows is to target hedgers, such as miners currently trading on CEXs, and provide a product that offers them ownership in the protocol through tokens while minimizing changes to their existing custody setups.

This strategy would mirror Babylon’s approach to acquiring users. When Babylon launched, there were already numerous offchain BTC-denominated hedge funds, and miners (some of the largest BTC holders) likely had access to them as liquidity providers. Babylon primarily bootstrapped trust through custodians and staking providers, particularly in Asia, meeting them where they were; it didn’t ask them to experiment with new wallets or key management systems filled with additional trust assumptions. Miners’ choice to adopt Babylon suggests they value either the ability to choose their own custody solution (whether self-custodial or with a different custodian), ownership via token incentives, or both. Otherwise, Babylon’s growth would be difficult to explain.

Now is a particularly opportune time to strike using this GTM. Coinbase’s recent acquisition of Deribit, the dominant CEX for options, represents a risk for foreign miners who may not want to hold large amounts of money in a U.S.-controlled entity. And innovations in the feasibility of BitVMs and overall quality of BTC bridges are unblocking the custody guarantees needed for an attractive onchain alternative.

Retail GTM: Offer Novel Trading Experiences

Rather than try and compete with perps at their own game of leverage, we believe the best way to attract retail is to offer retail novel products with simplified UX.

As discussed above, one of the most powerful features of options is the ability to take a direct view on volatility itself, independent of price direction. An onchain options protocol could build a vault on top of itself to allow retail users to go long/short volatility with simple UX.

Previous options vaults (like those on Dopex and Ribbon) suffered from unsophisticated quoting mechanisms, making them prone to losing money to arbitrageurs. But with the recent innovations in application-specific infrastructure we mentioned earlier, we have a clear “why now” that suggests you could build a vault that does not suffer from these issues. An options chain or rollup could leverage these advantages to improve execution quality for long/short volatility vaults while simultaneously bootstrapping liquidity/orderflow for the orderbook.

Conclusion

The conditions for onchain options to succeed are finally coming into place. Infrastructure has matured to support more capital-efficient designs, and onchain institutions now have genuine reasons to hedge directly onchain.

By building infrastructure that helps liquidity providers avoid bad orderflow and by anchoring around two price-insensitive user bases — hedgers seeking precision and retail seeking new trading experiences — onchain options protocols can finally build sustainable markets. With these foundations in place, options can become a core primitive of the onchain financial system in a way earlier attempts could not.

Thank you to Nick Forster (Derive), Jeff Anderson (STS), LTR (Delphi), the Kyan team (cozy, Marty, Beks), the Hyperdelta team (Ben, Ed), Dan Elitzer (Nascent), Ryan Unhedged (Racks.win), Ethan Brown (Balyasny), Cryptarbitrage (Deribit), E (Pye), Noah (Theia), NickH (Luxor), and Chris Pereira (U410).

1. Numbers are based on rough calculations with data from here and here.

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.

Disclaimer

All information contained herein is for general information purposes only. It does not constitute investment advice or a recommendation or solicitation to buy or sell any investment and should not be used in the evaluation of the merits of making any investment decision. It should not be relied upon for accounting, legal or tax advice or investment recommendations. You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment. None of the opinions or positions provided herein are intended to be treated as legal advice or to create an attorney-client relationship. Certain information contained in here has been obtained from third-party sources, including from portfolio companies of funds managed by Variant. While taken from sources believed to be reliable, Variant has not independently verified such information. Any investments or portfolio companies mentioned, referred to, or described are not representative of all investments in vehicles managed by Variant, and there can be no assurance that the investments will be profitable or that other investments made in the future will have similar characteristics or results. A list of investments made by funds managed by Variant (excluding investments for which the issuer has not provided permission for Variant to disclose publicly as well as unannounced investments in publicly traded digital assets) is available at https://variant.fund/portfolio. Variant makes no representations about the enduring accuracy of the information or its appropriateness for a given situation. This post reflects the current opinions of the authors and is not made on behalf of Variant or its Clients and does not necessarily reflect the opinions of Variant, its General Partners, its affiliates, advisors or individuals associated with Variant. The opinions reflected herein are subject to change without being updated. All liability with respect to actions taken or not taken based on the contents of the information contained herein are hereby expressly disclaimed. The content of this post is provided “as is;” no representations are made that the content is error-free.